Nobody Should Get Rich Off Obamacare

By Evan Soltas

Bloomberg View, December 3, 2013

For an industry that’s supposed to be burdened by the launch of Obamacare, the health-care business is doing pretty well. Stocks of health-care companies are up almost 40 percent this year, the strongest performance of any sector in the S&P 500.

How about the medical-technology manufacturers that were slapped with an excise tax? Doing just fine. The hospital chains that face lower reimbursement rates from Medicare patients? They’re doing well, too.

Health care is a business, and businesses are supposed to make money. Still, it’s a bit concerning that health-care investors are so upbeat just as President Barack Obama’s health-reform law goes into effect.

The law will give the insurance industry millions of new customers and subsidizes its products. It brings millions of others into the market for health-care services through its Medicaid expansion. If health-care investors are throwing a party, it might be because the rest of us are paying for it.

http://www.bloomberg.com/news/2013-12-03/nobody-should-get-rich-off-obamacare.html?alcmpid=view

Comment:

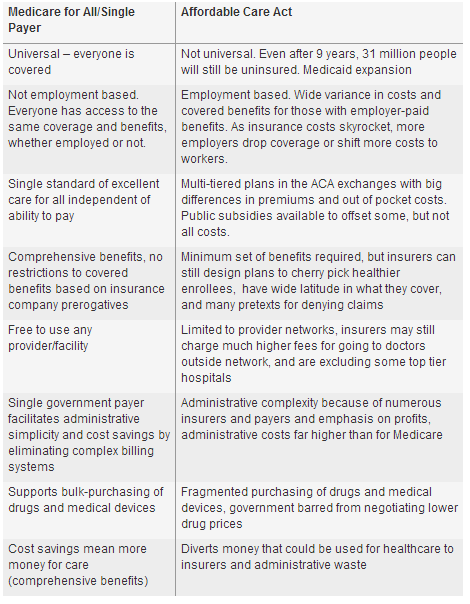

By Don McCanne, M.D. To pass the Affordable Care Act, President Obama was convinced that he had to gain the support of the health financing and health care industries. He did. Look who’s profiting. Who loses? Those who will have to pay much more out of pocket for health care because of higher deductibles. Those who lose choice of their physicians and hospitals because of narrower provider networks, and end up losing catastrophic protection because of care inadvertently received out of network. Those who will be contributing through taxes or insurance premiums far more than they should have to because of the profoundly wasteful administrative excesses of our dysfunctional financing system. That’s most of us. The improvements in insurance plans for the few – guaranteed issue and community rating – do not begin to offset the deterioration that is beginning to take place in the employer-sponsored plans where most of us receive our health care coverage. There are a few of us who will gain, some by being enrolled in Medicaid and some by receiving subsidies for exchange plans, but the numbers of us who will lose is far greater than the numbers who will win. We could have had reform in which we would all be winners – an improved Medicare that covers everyone. Even those who will gain through Medicaid or subsidies would gain much more under a single payer system. But no, political feasibility dictated that the vested stakeholders of the medical-industrial complex be the ones who get the money, while the rest of us pay more and get less.

]]>