http://www.oregonlive.com/news/oregonian/jack_ohman/

"Do no harm" by Jack Ohman

http://www.oregonlive.com/news/oregonian/jack_ohman/

Uwe Reinhardt on the public option

Who Needs the Public Option?

By Uwe Reinhardt

The New York Times

August 21, 2009

Nothing has been quite as riveting in recent media reports as the question of what President Obama and his staff really think…

How did the brouhaha over the choice of a public health plan come about in the first place, when the real issue before us has been helping the millions of currently uninsured, low-income American families gain access to adequate and reliable health insurance?

One would have hoped that the overarching goal of health reform would have been to put in place a reformed health insurance system that can offer Americans the same reliable, permanent, portable and life-cycle health insurance enjoyed by, say, Germans or Canadians or the people of Japan and Taiwan.

As I have argued in earlier posts to this blog, the choice of a public, government-run standard health insurance plan would certainly go a long way toward reaching that, but it is not a necessary condition for doing so. Germany, the Netherlands and Switzerland all do offer their citizens permanent, portable and stable financial security in health care without the inclusion of a government-run health plan in the mix. That achievement, however, requires fairly heavy regulation of the industry.

If I had to guess what features really make a public plan so attractive to many Americans, they would probably be the stability, permanence, portability and simplicity that such a public plan could offer. It is these features that make traditional, government-run Medicare so popular with the public.

Herein lies the main challenge facing the private health insurance industry. It must convince the public and the legislators who do not trust it that with the help of government — including a wide set of new government regulations — the industry can transform itself into a structure that can offer Americans the same permanent, reliable, easy-to-understand life-cycle financial security that citizens in other nations take for granted and Americans crave.

Thus, instead of the cliche that a public health plan would lead to a “government takeover of American health care” and thus its demise, the industry would be better advised to put before the public a fully worked out purely private-sector model that truly will offer individuals reliable, life-cycle health insurance with relatively stable premiums, and at premiums that are defensible.

http://economix.blogs.nytimes.com/2009/08/21/who-needs-the-public-option/

Comment:

The brouhaha over the public option is more than just symbolic. The accusation is correct: the public option was perceived as a means to move us toward single payer, while respecting the right of others to continue with their current coverage if they so preferred. The progressive camp was divided over this strategy since some of us believed that jettisoning single payer in favor of the public option would result in a bargaining position in which the public option would have to be traded away in exchange for some insurance market reforms. Those single payer advocates who agreed to support the public option now feel betrayed.

But the much more important goal is to establish a system that prevents financial hardship for anyone who needs health care – a system of social insurance, whether that is based on single payer or on a system of highly regulated private plans, as some European nations have.

Congress is trying to patch together a model based on private plans, but they have run up against a uniquely American problem – our very high health care costs. The average health care cost far a healthy family of four (the healthy workforce and their young healthy families) is now $16,771. With a typical family income of $60,000, generous subsidies will be mandatory for middle-income individuals and families.

We already have hit the wall on costs. Congress is proposing basic coverage (tier one) that has an actuarial value of 65 to 70 percent, leaving those with significant health care needs exposed to the balance of the costs (which is often higher than the stop loss because of the failure of our private insurance model to protect individuals from unanticipated out-of-network charges). Average-income individuals who need care will not be able to afford the out-of-pocket costs.

Even for those who remain healthy, our costs are now so high that a plan with reasonable benefits that would provide adequate financial protection in the event of need must charge premiums that are so high that a generous public subsidy is essential. The wall again – Congress is unwilling to use aggressive, progressive tax policies to pay for subsidies that are large enough to keep premiums affordable for average-income individuals.

There is an out. Congress will waive the fine for the criminal act of being uninsured merely because the premium is unaffordable. The standard “coverage” for the middle-income sector will then be “hardship waivers” (assuming a transition away from employer-sponsored coverage – the intent of many members of Congress). The only other option besides aggressive tax policies would be to make the basic plan so Spartan that it won’t provide adequate financial protection anyway. (Don’t say high deductible plans, because if the deductible is high enough to make the premium affordable, the plans do not provide adequate protection for middle-income individuals and families.)

The real problem with the public option concept is that it automatically leaves in place the most expensive and least efficient method of financing health care. A single payer or improved Medicare for all would provide us with more than simply an equitable and efficient method of financing care for everyone, it would also create our own public monopsony so that we can demand greater value from our health care system.

Joe Scarborough Is Shocked, Yet Awed by Single-Payer Logic

By Leslie Savan

The Nation

08/20/2009

Something rather remarkable happened on Tuesday’s Morning Joe. Rep. Anthony Weiner of New York pointed out that the health insurance industry has no clothes, and Joe Scarborough, after first trying to spin it some gossamer threads, broke down and said, By God, you’re right, this emperor is a naked money-making machine!

Well, he didn’t use those exact words, but Joe did seem to finally get that America has granted insurance companies the right to create bottlenecks in the financing of healthcare in order to extract profits out of the suffering of ordinary people–without providing any actual healthcare whatsoever.

“Why are we paying profits for insurance companies?” Weiner asked Scarborough. “Why are we paying overhead for insurance companies? Why,” he asked, bringing it all home, “are we paying for their TV commercials?”

Weiner, who recently warned that President Obama could lose as many as 100 votes on a health bill if a public option is not included, really wants single payer–Medicare for all Americans is his goal. What a crazy, way-out, reckless notion, Joe went into their encounter believing. But Weiner asked some simple, direct questions that no politician, much less Obama or HHS Secretary Kathleen Sebelius, has managed to pose:

What is an insurance company? They don’t do a single check-up. They don’t do a single exam, they don’t perform an operation. Medicare has a 4 percent overhead rate. The real question is why do we have a private plan?

“It sounds like you’re saying you think there is no need for us to have private insurance in healthcare,” Joe asked at one point.

Weiner replied: “I’ve asked you three times. What is their value? What are they bringing to the deal?”

Scraping the bottom of a seemingly bottomless pit of spin, Joe is repeatedly left speechless, “stunned” and “astounded,” he said, by the questions themselves. Indeed, when confronted with unfettered capitalism’s massive failures, the right usually has nothing to say. The “free market” is supposed to eternally grow, not crash under its own greed. They’re left ideologically crippled.

But unlike, say, Lou Dobbs, who began dobbering when confronted with similarly direct argument for single-payer, Joe was able to take a deep breath and return from a break with his eyes opened.

He even repeated Weiner’s points clearly: The goverment would take over only the “paying mechanism” of healthcare, not the doctors or their medical decisions themselves. His ears perked up every time Weiner mentioned that the nonprofit Medicare spends 4 percent on overhead, while private insurers spend 30 percent.

And Joe, who has been criticizing mob rule at town halls, seemed to appreciate the way Weiner counters the fearmongering over Medicare: After decades of railing against the program’s wasteful, “runaway” spending, Republicans have done a 180 and are now trying to scare seniors that the Democrats’ proposed Medicare cuts will come directly from their medical care and not, as is actually proposed, from wasteful, stupid practices in the system–like, as Weiner mentions, putting people into a $700-a-night hospital bed when all they really need, and often prefer, is a visit by a homecare attendant in the two-digit-a-day range.

Maybe the real turning point came when Weiner asked, “How does Wal-mart offer $4 prescriptions?” Joe and co-host Mika Brzezinski looked as if they’d been thwacked by a hardback copy of Atlas Shrugged, and sat back to let the congressman explain it all to them:

They go to the pharmaceutical companies and say, “Listen, we have a giant buying pool here. You’re going to give us a great deal.”

Who’s bigger than Wal-Mart? We are, the taxpayers. Do we do that? No. Because we have outsourced this to insurance companies who don’t have necessarily as much incentive to keep those costs down because, frankly, they are getting a piece of the action.

Progressives tend to understand this stuff, but many conservatives won’t trust such logic, especially in the abstract, which is how most Dems have been communicating. But Weiner, aware that if you can’t visualize something it ain’t going to stick, argued with a specific, familiar visual–that of a successful, supercapitalist, and, as Mika might say, “real American” company. And suddenly, as the mote dropped from the MJ crew’s eyes, Weiner went from “scaring American citizens,” in Joe’s words, to instant celeb.

“That was SO great!” said Mika, as she and Joe asked Anthony to please, please come back soon, this week if possible!

“You have succeeded in doing something that no one else has done on this show in two years,” said Joe, his fists rapidly knocking the table in excitement. “You made me speechless. And you made me speechless because you so clearly came here and stated your position.”

While maintaining that he and Weiner have “different worldviews,” Joe nevertheless raved, “This is fascinating, and one of the problems with the president’s message is that it’s muddled.” And, damn, that’s true.

Could this episode herald a Single-Payer Awakening? Or is this just the thrill of logic running up Joe’s leg, soon to be forgotten as corporate media try to undermine real reform of a system that feeds the nets millions in ad revenue? When the big mainstream players shouted in unison to prematurely declare the public option dead, I couldn’t help but think: In the corporate media’s total takeover of ideas, they, too, have a death panel–made up of three or four conglomerate owners and chaired by Rupert Murdoch–that will determine whether an idea lives or gets its plug pulled.

On Thursday, Morning Joe replayed Weiner’s best hits, but Joe was occasionally dobbering himself, complaining that our healthcare problems come down to costs, costs, costs but “now all the President is talking about is a moral imperative.” (Of course, Obama put morality on the table only yesterday; until then, he focused on costs, costs, costs.)

We’ll see how far this relative openness to single-payer goes. In the meantime, though, the education of Joe Scarborough is, as always, a sight to behold:

Anthony Weiner Leaves Scarborogh "Speechless"

Rep. Anthony Weiner on MSNBC

August 18, 2009

Anthony Weiner Leaves Scarborogh “Speechless”

Rep. Anthony Weiner on MSNBC

August 18, 2009

Concerns about reform efforts

NBC News Health Care Survey

Hart/McInturff

August 15-17, 2009

8. Thinking about efforts to reform the health care system, which would concern you more?

41% – Not doing enough to make the health care system better than it is now by lowering costs and covering the uninsured.

54% – Going too far and making the health care system worse than it is now in terms of quality of care and choice of doctor.

5% – Not sure

http://msnbcmedia.msn.com/i/MSNBC/Sections/NEWS/NBC-WSJ_Poll.pdf

Comment:

By Don McCanne, MD

A PhD thesis could be written over just what this survey tells us, but we’re certainly not going to do that here.

Give this some thought. Think about what this might mean. Then think about what we should be doing in response. And then do it!

New Harvard study reveals that taxing job-based health benefits would hit working families hardest

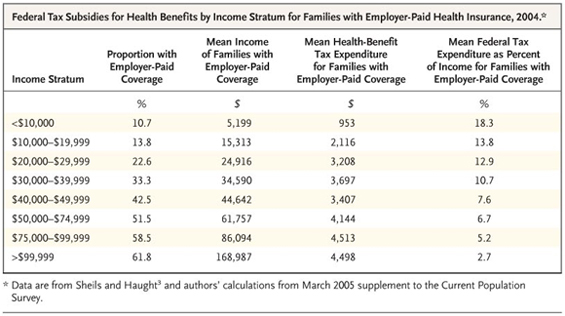

Income and insurance data show that insured, working-poor families would be taxed 140 times more than Wall Street execs

FOR IMMEDIATE RELEASE

August 20, 2009

Contacts:

David Himmelstein, M.D.

Steffie Woolhandler, M.D., M.P.H.

Mark Almberg, Physicians for a National Health Program, (312) 782-6006, mark@pnhp.org

CAMBRIDGE, Mass. – As the debate over health care reform continues to unfold in town hall meetings and on Capitol Hill, a new study by two Harvard researchers has found that taxing job-based health benefits would heavily penalize insured, working families.

The study, titled “The regressivity of taxing employer-paid health insurance,” appears in the August 19 online edition of the New England Journal of Medicine. It was written by Drs. David Himmelstein and Steffie Woolhandler, professors at Harvard Medical School and primary care doctors at Cambridge Hospital in Massachusetts.

The taxation of employer-sponsored health benefits has been advocated by many health economists and lawmakers, including some members of the influential Senate Finance Committee, which is now drafting health care reform legislation. President Obama has said he has not ruled out such a tax to fund his reforms.

Analyzing income and insurance data from the 2005 Current Population Survey of the U.S. Census Bureau and other sources, the authors reveal that taxing workers’ job-based health insurance would cost those with low-incomes ($0- $10,000 annually) 18.3 percent of their income, but cost high-income (over $100,000) families a mere 2.7 percent. (See the table from the study at http://healthcarereform.nejm.org/?p=1521)

The authors note that the tax rate would drop even lower for the super-rich. “A Goldman Sachs executive who enjoyed the firm’s infamous $40,543 health plan got a federal tax subsidy of about $15,367 last year,” they write. “But that’s only 0.13 percent of the bonuses received by the company’s four top earners. So though taxing health benefits would spare the uninsured, the average poor family with employer-paid coverage would be taxed at a rate 140 times higher than Wall Street titans.”

Dr. David U. Himmelstein, lead author of the study and associate professor of medicine at Harvard, added: “Most economists and many politicians have claimed that taxing health benefits would hit the wealthy hardest, while sparing the poor. But exactly the reverse is true. For a poor, insured family a tax on their health benefits would take almost one-fifth of their total income.”

Dr. Steffie Woolhandler, co-author and professor of medicine at Harvard, said: “Instead of taxing benefits, politicians should embrace the only affordable option for universal coverage: a single-payer, Medicare-for-all program. Single-payer would save $400 billion annually by simplifying administration, enough to assure quality care for everyone. We cannot afford to keep wasteful private health insurers in business, and pay for it off the backs of working families.”

Himmelstein and Woolhandler are co-founders of Physicians for a National Health Program, an organization of 16,000 doctors and medical professionals who advocate for single-payer national health insurance.

*******

A copy of the study is available from the New England Journal website at http://healthcarereform.nejm.org/?p=1521

“The Regressivity of Taxing Employer-Paid Health Insurance,” David U. Himmelstein, M.D; Steffie Woolhandler, M.D., M.P.H. New England Journal of Medicine, August 19, 2009.

Drs. Himmelstein and Woolhandler are available for comment on their new study and on other aspects of the health care reform debate. To contact other physician-spokespersons from Physicians for a National Health Program in your area, visit www.pnhp.org/stateactions or call (312) 782-6006.

"Pre-Existing Condition" by Jim Morin

http://www.miamiherald.com/opinion/jim-morin/

“Pre-Existing Condition” by Jim Morin

http://www.miamiherald.com/opinion/jim-morin/

Policies to address out-of-network charges

Code Blue: Out-of-Network Charges Can Spur Financial Emergency

By Paul Raeburn

Kaiser Health News

August 19, 2009

On the evening of March 1, 2008, Gary Diego was relaxing with his wife, Ellen, when she abruptly lost her hearing, began repeating herself, and seemed to be losing her grip.

Alarmed, Diego rushed her to his insurance company’s in-network hospital, near his home in Truckee, Calif. Unable to handle what was determined to be bleeding in the brain, the hospital quickly transferred her to Renown Regional Medical Center in Reno, Nev., where she spent 17 days in intensive care. While recovering, she caught pneumonia and died.

A few weeks later, a still-grieving Diego learned from his insurer, Health Net, that he owed the Reno hospital $75,462.77. The reason? The hospital was not in his approved network.

(Later Mr. Diego paid a medical billing consultant $7,500 to negotiate a settlement.)

http://www.kaiserhealthnews.org/Stories/2009/August/19/out-of-network.aspx

And…

Tackling the Mystery of How Much It Costs

By Gina Kolata

The New York Times

August 18, 2009

But the health care legislation under discussion does not directly address the out-of-network fee issue. And that is intentional, says Dr. Mark McClellan of the Brookings Institution. Dr. McClellan, a former head of Medicare who works closely with policy makers, says the goal of the House and Senate bills is to encourage people to stay in their networks. He added that the result should be networks that provide better care “so that people don’t have so much need to go outside of them.”

Mark A. Hall, a professor of law and public health at Wake Forest University, for example, advocates restricting out-of-network fees to a fixed amount, perhaps 150 percent of the amount Medicare would pay.

That is how the system works in Germany, says Uwe Reinhardt, a health economist at Princeton University. Professor Reinhardt advocates a national law that caps the maximum doctors can charge when they are out of a patient’s network.

America’s Health Insurance Plans, which represents health insurers, is also trying to draw attention to out-of-network doctors’ fees. Last Tuesday, the group released results of its own survey to show how high such fees can go.

Jonathan Gruber, a health economist at M.I.T., says, however, that it makes more sense to encourage people to stay in networks.

Some may want to pay anyway for an out-of-network doctor, and that is fine, he said. “If you want to go outside your network, God bless you,” he said. “It’s the American way.”

But the only way to fix the system, Dr. Gruber said, is to make the networks better so that people will stay in them and then, most patients, knowing what it will cost them to leave their networks, will decide not to.

http://www.nytimes.com/2009/08/19/health/policy/19fees.html

qotd on AHIP’s report referenced above:

https://pnhp.org/news/2009/august/ahip_explains_why_pr.php

Comment:

By Don McCanne, MD

What are private insurers selling us? Their primary product is a network of health care providers that have contracted to accept the insurers’ rates. The benefit of that is that it has helped to slow the rate of increase in health insurance premiums. One major problem with that is individuals frequently obtain care from out-of-network providers – usually not by choice, but by medical circumstances not really under the control of the patient. Under most insurance plans, the individual then becomes responsible for payment of most or all of the out-of-network charges.

With higher premiums, larger deductibles, greater coinsurance, more benefit exclusions, patients are already facing financial hardship without the addition of the out-of-network charges. These unanticipated charges are contributing to our growing epidemic of underinsurance. What to do?

Mark McClellan (think of Medicare privatization) and Jonathan Gruber (think of Massachusetts’ flawed policy of getting more people covered and then pretending that we can figure out later on how to make it work) both believe the answer is to penalize individuals who obtain out-of-network care in an effort to establish incentives for insurers to create perfect networks so that out-of-network care will never have to happen. Of course, “it’s the American way” to choose care outside of your network, and “God bless you” when you can’t pay your bills.

It’s also the American way for Mr. Diego to receive a $75,000 out-of-network bill for his wife’s life-threatening and life-ending care. Haven’t we had enough of our uniquely American system?

There is another way of protecting patients from out-of-network charges. The government can require that out-of-network fees be close to insurer-authorized payments within networks. Yes, that would be the imposition of government fee controls, but fees that are designed to match fees already imposed by the private insurer bureaucracies. That would help, but it does bring up an important question. If the government is going to impose fee controls anyway, then why should we continue to pay the costs of the outrageous administrative waste of the private insurers?

Some might say that they do provide us with the function of pooling risk. But one of the goals of reform is to pool risk across insurers, relieving them of the burden of bearing risk. If we achieve risk equalization then it would be much more efficient and equitable to establish a single universal risk pool administered by the government. Again, the private insurers would be superfluous.

How much risk are the insurers exposed to now under our current system? Half of employer-sponsored benefits are already self-insured. The employer pays the benefits with absolutely no risk exposure to the insurers. So what do the insurers provide the employer? Claims processing for one. But the other service should really give us pause. The private insurers rent their network provider lists to the self-insured employers. How many physicians do you think might be offended if they knew that rent was being paid for use of contracts they signed with the insurers that require the physicians to provide a large discount, and that rent is not going to the physicians but is being kept by the private insurers!?

Tell Congress and the President that we’ve had it with private insurers! Urge them to support the single-payer amendment to the House bill by Rep. Anthony Weiner which Speaker Pelosi has promised will receive an up or down vote on the House floor this year.

Use the following link to access resources on the Weiner amendment:

https://pnhp.org/amendment/

Physician-patient relationship should be sacrosanct

By Syed Quadri

Guest columnist

The News Enterprise (Elizabethtown, Ky.)

I have watched with interest the debate over health care reform unfold in the columns of your newspaper and the rest of media. The airways and the pages of every newspaper in the country are saturated with several buzzwords. “Rationing,” “socialized medicine,” “federal bureaucracy,” and “government takeover of health care” are the names that appear to be driving the discussion and creating the frame of reference for the “debate.”

Allow me to share with your readers my experience with the health care system relative to one concern, of increased federal bureaucratic interference, that has been expounded by the opponents of President Barack Obama’s plan to reform the health care system.

I am a general internist and have been practicing internal medicine in Hardin County for the past 11 years. As an internist I specialize in treating medical conditions of adults and especially the elderly. About 50 percent of my patients are covered by Medicare, and the rest have private insurance, Medicaid or self-pay. I am sure everybody is aware that Medicare is a government program operated by the federal bureaucratic agency of the centers of Medicare and Medicaid services.

I have had approximately 30,000 clinical encounters involving patients with Medicare insurance, and the decisions made during these medical visits were never, not even on a single occasion, questioned or rejected by federal bureaucrats. Never has the shadow of a federal bureaucrat even remotely intruded on the intimate space of the physician-patient engagement. I have the full freedom and Medicare patients have the full freedom and broad choice to avail of all reasonable medical tests and pursue necessary treatment without seeking anybody’s permission.

In contrast, the clinical encounters involving patients with private insurance are different. Many of the clinical decisions that result from that encounter are scrutinized, some are rejected by the insurance company, many are grudgingly accepted but only after considerable effort and time has been expended in explaining and convincing the corporate lackeys the merits of doing a test or prescribing a treatment.

When I decide to order an MRI scan of the knee for a Medicare beneficiary to explore for a cartilage tear, my office staff simply schedules the test. On the the other hand, in that same situation, every private insurance company requires that permission be obtained for the test to be done. A corporate bureaucrat can deny the test a doctor has deemed necessary.

It takes me two minutes to admit a Medicare beneficiary to the hospital from my office and up to two hours to admit a patient with private insurance with that amount of time required to obtain permission from the insurance company’s clerk. Once the patient is admitted to the hospital the continued need for hospitalization will be determined not by the doctor but by corporate bureaucrats.

The core principle of medicine is that the physician-patient relationship is sacrosanct and no other agency or entity should attempt to intrude into this special ground or endeavor to influence, alter or abridge the decision that a patient and physician arrive at after an informed discussion. Among insurances only Medicare, an entity managed by federal bureaucrats, honors and abides by this principle, while the denizens of blue-blooded corporate America in their various insurance incarnations with no regard to medical ethics or any ethics trample upon this ideal every day.

The public should rightly be incensed at any effort by a third party to intrude into the privileged realm of a medical transaction or hinder the ability of the physician to freely exercise his professional judgment, but the outrage would be misdirected if it is aimed at the federal bureaucracy. Contrary to popular belief it is not government bureaucrats who seek to restrict the freedom of the patients and physicians alike but it is their counterparts in the private health insurance sector who relentlessly seek to modify, abbreviate and at times nullify a physician’s considered opinion that was formulated in the best interest of his patient.

Surprisingly the shenanigans of the private health insurance bureaucracy have escaped the public’s attention while the phantoms of federal bureaucratic interference have captured the popular imagination. I hope that public opinion will be infused by the bright light of facts and not be inflamed by the passionate heat of irrational emotions in discussing this important issue of health care reform.

Syed Quadri MD, FACP, has practiced internal medicine in Hardin County for 11 years.