http://www.boston.com/bostonglobe/editorial_opinion/dan_wasserman_cartoonist/

Sen. Daschle’s “Critical”

Critical: What We Can Do About the Health-Care Crisis

By Senator Tom Daschle, with Scott S. Greenberger and Jeanne M. Lambrew

Thomas Dunne Books, February 2008

The key question for any health-care reform plan is, “How will it cover people?” Most of the world’s highest-ranking health-care systems employ some kind of “single-payer” strategy – that is, the government, directly or through insurers, is responsible for paying doctors, hospitals, and other health-care providers. Supporters say single-payer is brilliantly simple, ensures equity by providing all people with the same benefits, and saves billions of dollars by creating economies of scale and streamlining administration. But pure single-payer system is politically problematic in the United States, at least right now. Even though polls show that seniors are happier with Medicare than younger people are with their private insurance, opponents of reform have demonized government-run systems as “socialized medicine.”

I have strong views on what an “ideal” system would look like. But I’m not willing to sacrifice worthy improvements on the altar of perfection. I find it encouraging that the leading Democratic presidential contenders appear to share this attitude. The proposals that Obama, Clinton, and Edwards put forward would improve our current system rather than scrapping it, using the Massachusetts reform plan as a model.

The Federal Health Board

I believe a Federal Health Board should be charged with establishing the system’s framework and filling in most of the details. This independent board would be insulated from political pressure and, at the same time, accountable to elected officials and the American people.

First, it would set the rules for the expanded FEHBP, placing conditions on the private insurers wishing to participate.

Second, the Federal Health Board would promote “high-value” medical care by recommending coverage of those drugs and procedures backed by solid evidence.

A third function of the Federal Health Board would be to align incentives with high-quality care.

Finally, the Federal Health Board might also play a role in rationalizing our health-care infrastructure.

http://us.macmillan.com/critical

Comment:

By Don McCanne, MD

When it was announced that Tom Daschle was Barack Obama’s choice to be Secretary of Health and Human Services, it was also announced that he would not only be an administrator, but also he would lead the team that is crafting the definitive health care reform proposal for the Obama administration. That is why Sen. Daschle’s book, “Critical,” is important to us. It provides us with the views of the person who will be working with Congress to reform our health care system.

The fundamentals of his proposal are essentially the same as those proposed by Barack Obama, Max Baucus, and most of the other Democrats who have been advocating for reform. He would continue employer-sponsored coverage, expand public programs, and provide an FEHBP-type program, including a Medicare-like option. He would attempt to achieve universal coverage through an individual mandate with financial assistance for lower-income individuals.

Daschle also includes other concepts that are making the political rounds, such as information systems, community health centers, quality measurements, and “shared responsibility.”

One essential reform that seems to be missing from his proposal is the need to reinforce our primary care infrastructure, providing everyone with a medical home. Maybe that could be extrapolated from his call for rationalizing our health care infrastructure, but, if so, it is of such great importance that he should advocate for it explicitly.

What is relatively unique in Daschle’s proposal is the recommendation for a Federal Health Board, based on a model similar to the Federal Reserve System. One of the more important functions would be to provide oversight of the private insurance industry in his multi-payer system, a role that would be unnecessary in a single payer system. The other functions he describes can easily be or already are provided by existing agencies, though introduction of a single payer system would certainly be accompanied with appropriate bureaucratic reform.

Although he recommends that this board be quasi-independent, insulated from political influence, there is still risk that ideological extremists could gain control. Think of the failure of the Federal Reserve System to provide adequate oversight of our financial system, contributing to our current financial meltdown. That might not have occurred if free-market ideologues such as Alan Greenspan had not been in charge of the Federal Reserve. The Supreme Court is also insulated from political interference, yet obviously it too is controlled by ideologues, over whom we have no control. Imagine if we had a Federal Health Board composed of those individuals who, through the Medicare Modernization Act, damaged our public Medicare program. If they had been in control of such a board, we could have been much further down the road toward their goal of a totally privatized Medicare system.

Most troubling is Sen. Daschle’s conclusions on single payer. He describes it as the model used by the “world’s highest-ranking health care systems.” He acknowledges, without dispute, that supporters say that it is “brilliantly simple, ensures equity by providing all people with the same benefits, and saves billions of dollars by creating economies of scale and streamlining administration.” Yet he rejects it merely because it is “politically problematic.” He would sacrifice the “ideal” system because he is “not willing to sacrifice worthy improvements on the altar of perfection.”

It certainly is true that opportunities for enacting beneficial policies can be missed when the politics are not in alignment. But it is also true that bringing the politics into alignment can eliminate the opportunity to enact ideal policies. For success in achieving a high-performance health care system, we shouldn’t sacrifice policy; we should change the politics.

Why Does U.S. Health Care Cost So Much? (Part III: An Aging Population Isn’t the Reason)

By Uwe E. Reinhardt

New York Times

December 5, 2008

Graphs courtesy of Uwe Reinhardt.

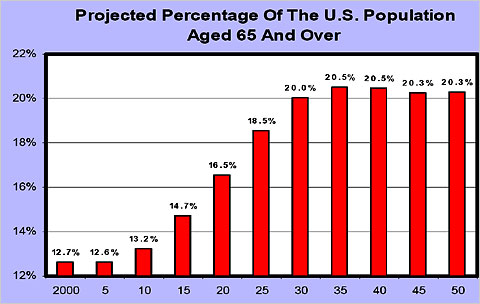

Not a conference on health care goes by without someone’s asserting that the aging of our population is a major driver of the annual growth in health spending. It sounds intuitively appealing if one contemplates the following two graphs, which are regularly trotted out on such occasions.

The first graph depicts what is commonly described as the “Baby Boom Tsunami.” The second depicts age-specific health spending per capita in 1999, relative to the spending of Americans in the age group 35 to 44, which is set to 1. These age-specific relative spending profiles do not change much over time for a given country, and they do not much differ among industrialized nations. They show that after age 60 or so, health spending per capita rises sharply with age.

Yet, research around the world has shown that the process of the aging of the population by itself adds only a very small part — usually about half a percentage point — to the annual growth in per-capita health spending in industrialized societies, which tends to range between 5 and 8 percent, depending on the country and the period in question. The bulk of annual spending growth can be explained by overall population growth (about 1.1 percent per year), increases in the prices of health care goods and services, and the availability of ever more new, often high-cost medical products and treatments used by all age groups.

Because this proposition is so counterintuitive, readers may wish to consult two recent research papers on the topic, one penned by the present author, and the other penned by other researchers.

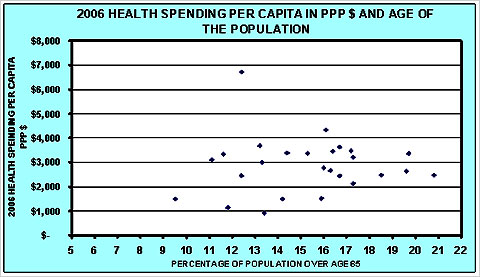

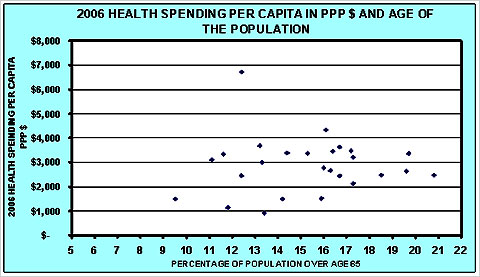

These papers are based on American data. Similar studies have appeared also for Canada, Australia and many other countries in the Organization for Economic Cooperation and Development. Indeed, it may surprise readers that knowing the percentage of a nation’s population that is over age 65 cannot help one explain cross-national differences in health spending per capita, as is shown in the graph further on. As the graph shows, the per-capita health spending of nations is virtually independent of the age structure of its population.

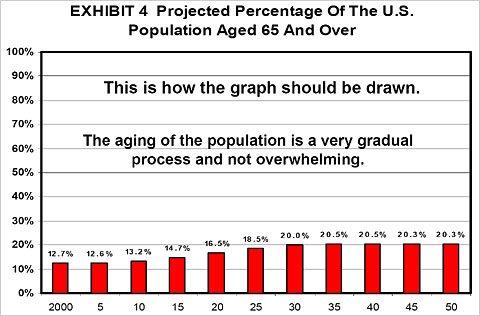

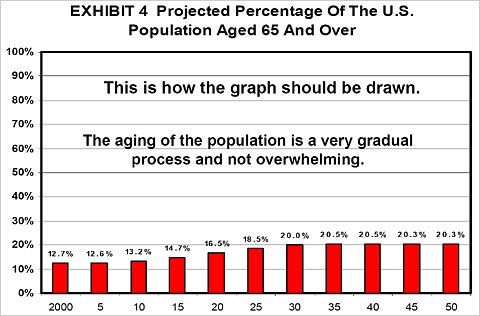

Why, then, is the aging of the population such a small driver of annual increases in health spending? The answer can be found in the last graphical display of this commentary. That graph contains the same data as the first graph in this commentary, but the vertical axis is scaled as it should be scaled: from 0 percent to 100 percent. Letting it run from 12 percent to 22 percent stretches the vertical axis and creates the image of the famous Baby Boom Tsunami. It is a form of lying with statistics.

As this graph illustrates, the aging of our population is a very gradual process and does not come even close to resembling a tsunami. It is at best a demographic ripple.

Furthermore, current population projections have the fraction of elderly in the United States population peak at around 20 percent. Along with Canada and Australia, we shall be for a very long time the youngest nation in the O.E.C.D. Only in 2025 will the American population be as “old” as many European populations are already today.

As the song goes, relative to other nations we shall be “forever young”!

Uwe E. Reinhardt is an economist at Princeton.

Sen. Daschle's "Critical"

Critical: What We Can Do About the Health-Care Crisis

By Senator Tom Daschle, with Scott S. Greenberger and Jeanne M. Lambrew

Thomas Dunne Books, February 2008

The key question for any health-care reform plan is, “How will it cover people?” Most of the world’s highest-ranking health-care systems employ some kind of “single-payer” strategy – that is, the government, directly or through insurers, is responsible for paying doctors, hospitals, and other health-care providers. Supporters say single-payer is brilliantly simple, ensures equity by providing all people with the same benefits, and saves billions of dollars by creating economies of scale and streamlining administration. But pure single-payer system is politically problematic in the United States, at least right now. Even though polls show that seniors are happier with Medicare than younger people are with their private insurance, opponents of reform have demonized government-run systems as “socialized medicine.”

I have strong views on what an “ideal” system would look like. But I’m not willing to sacrifice worthy improvements on the altar of perfection. I find it encouraging that the leading Democratic presidential contenders appear to share this attitude. The proposals that Obama, Clinton, and Edwards put forward would improve our current system rather than scrapping it, using the Massachusetts reform plan as a model.

The Federal Health Board

I believe a Federal Health Board should be charged with establishing the system’s framework and filling in most of the details. This independent board would be insulated from political pressure and, at the same time, accountable to elected officials and the American people.

First, it would set the rules for the expanded FEHBP, placing conditions on the private insurers wishing to participate.

Second, the Federal Health Board would promote “high-value” medical care by recommending coverage of those drugs and procedures backed by solid evidence.

A third function of the Federal Health Board would be to align incentives with high-quality care.

Finally, the Federal Health Board might also play a role in rationalizing our health-care infrastructure.

http://us.macmillan.com/critical

Comment:

By Don McCanne, MD

When it was announced that Tom Daschle was Barack Obama’s choice to be Secretary of Health and Human Services, it was also announced that he would not only be an administrator, but also he would lead the team that is crafting the definitive health care reform proposal for the Obama administration. That is why Sen. Daschle’s book, “Critical,” is important to us. It provides us with the views of the person who will be working with Congress to reform our health care system.

The fundamentals of his proposal are essentially the same as those proposed by Barack Obama, Max Baucus, and most of the other Democrats who have been advocating for reform. He would continue employer-sponsored coverage, expand public programs, and provide an FEHBP-type program, including a Medicare-like option. He would attempt to achieve universal coverage through an individual mandate with financial assistance for lower-income individuals.

Daschle also includes other concepts that are making the political rounds, such as information systems, community health centers, quality measurements, and “shared responsibility.”

One essential reform that seems to be missing from his proposal is the need to reinforce our primary care infrastructure, providing everyone with a medical home. Maybe that could be extrapolated from his call for rationalizing our health care infrastructure, but, if so, it is of such great importance that he should advocate for it explicitly.

What is relatively unique in Daschle’s proposal is the recommendation for a Federal Health Board, based on a model similar to the Federal Reserve System. One of the more important functions would be to provide oversight of the private insurance industry in his multi-payer system, a role that would be unnecessary in a single payer system. The other functions he describes can easily be or already are provided by existing agencies, though introduction of a single payer system would certainly be accompanied with appropriate bureaucratic reform.

Although he recommends that this board be quasi-independent, insulated from political influence, there is still risk that ideological extremists could gain control. Think of the failure of the Federal Reserve System to provide adequate oversight of our financial system, contributing to our current financial meltdown. That might not have occurred if free-market ideologues such as Alan Greenspan had not been in charge of the Federal Reserve. The Supreme Court is also insulated from political interference, yet obviously it too is controlled by ideologues, over whom we have no control. Imagine if we had a Federal Health Board composed of those individuals who, through the Medicare Modernization Act, damaged our public Medicare program. If they had been in control of such a board, we could have been much further down the road toward their goal of a totally privatized Medicare system.

Most troubling is Sen. Daschle’s conclusions on single payer. He describes it as the model used by the “world’s highest-ranking health care systems.” He acknowledges, without dispute, that supporters say that it is “brilliantly simple, ensures equity by providing all people with the same benefits, and saves billions of dollars by creating economies of scale and streamlining administration.” Yet he rejects it merely because it is “politically problematic.” He would sacrifice the “ideal” system because he is “not willing to sacrifice worthy improvements on the altar of perfection.”

It certainly is true that opportunities for enacting beneficial policies can be missed when the politics are not in alignment. But it is also true that bringing the politics into alignment can eliminate the opportunity to enact ideal policies. For success in achieving a high-performance health care system, we shouldn’t sacrifice policy; we should change the politics.

HMS Sees Inequity in Organ Donations

Uninsured patients 20 times more likely to donate an organ than to receive one

By DANIELLE J. KOLIN

The Crimson

Contributing Writer

12/5/2008

Americans who lack health insurance are about 20 times more likely to donate a liver or kidney than to receive one, according to a new study by researchers at Harvard Medical School.

The findings, published in the latest issue of the International Journal of Health Services, show that 17 percent of organ donors did not have health insurance in 2003, while only 0.8 percent of organ recipients were uninsured.

“It’s a way of highlighting how unfair what goes on in our health care system is,” said Medical School Professor David U. Himmelstein, one of the study’s authors. “It’s immoral what we’re doing. Everybody should have insurance.”

The lead author of the study, Andrew A. Herring, was a third-year student at the Medical School when he treated a 25-year-old uninsured day laborer suffering from cardiomyopathy. When the patient died from lack of a heart transplant, Herring was inspired to explore the role of insurance coverage in whether or not a patient can receive an organ.

“People donate irrespective of their insurance,” said Herring, who is now doing a residency in emergency medicine in Oakland, Calif. “They donate from an altruistic sense of wanting to help someone else. Out of respect for that motive, the health care system needs to reflect the same altruism, which means allocation of organs irrespective of ability to pay.”

The authors made their conclusions by analyzing data from the 2003 National Inpatient Sample, a random representative sample of hospital stays.

The doctors emphasized that the discrepancy between organs received by the uninsured and the insured does not reflect the “values or intentions of the transplant community.”

“The vast majority of transplant surgeons want to give organs to those who get the greatest benefit from them, but the system around them is failing them,” Herring said.

According to the study, the discrepancy is due to the expensive post-surgical care required after organ transplantation. For successful organ transplantation, the patient must undergo long-term immunosuppressive therapy. If the patient is unable to pay–and uninsured patients seldom are–the transplantation is less likely to succeed.

Himmelstein and the paper’s third author, Medical School Professor Stephanie J. Woolhandler, are the co-founders of Physicians for a National Health Program, an organization dedicated to supporting a universal, single-payer national health system.

“My hope is that papers like this are part of a growing consensus that a universal health care system is necessary,” Herring said.

Himmelstein said that the study represents additional evidence to support such a health care system, and he criticized President-elect Barack Obama’s health insurance reform proposals for not going far enough because it continues to rely on private health insurance companies.

“Unfortunately, what’s being proposed by President-elect Obama and the leading Democrats is very disappointing,” Himmelstein said. “We know that it won’t work.”

Programs similar to the Democratic proposal have been tried at least five times previously at the state level, Himmelstein said, and have always failed.

“It makes good politics but it’s economically nonsensical to say we’ll rely on the private health insurance industry,” Himmelstein said.

Why Does U.S. Health Care Cost So Much? (Part III: An Aging Population Isn't the Reason)

By Uwe E. Reinhardt

New York Times

December 5, 2008

Graphs courtesy of Uwe Reinhardt.

Not a conference on health care goes by without someone’s asserting that the aging of our population is a major driver of the annual growth in health spending. It sounds intuitively appealing if one contemplates the following two graphs, which are regularly trotted out on such occasions.

The first graph depicts what is commonly described as the “Baby Boom Tsunami.” The second depicts age-specific health spending per capita in 1999, relative to the spending of Americans in the age group 35 to 44, which is set to 1. These age-specific relative spending profiles do not change much over time for a given country, and they do not much differ among industrialized nations. They show that after age 60 or so, health spending per capita rises sharply with age.

Yet, research around the world has shown that the process of the aging of the population by itself adds only a very small part — usually about half a percentage point — to the annual growth in per-capita health spending in industrialized societies, which tends to range between 5 and 8 percent, depending on the country and the period in question. The bulk of annual spending growth can be explained by overall population growth (about 1.1 percent per year), increases in the prices of health care goods and services, and the availability of ever more new, often high-cost medical products and treatments used by all age groups.

Because this proposition is so counterintuitive, readers may wish to consult two recent research papers on the topic, one penned by the present author, and the other penned by other researchers.

These papers are based on American data. Similar studies have appeared also for Canada, Australia and many other countries in the Organization for Economic Cooperation and Development. Indeed, it may surprise readers that knowing the percentage of a nation’s population that is over age 65 cannot help one explain cross-national differences in health spending per capita, as is shown in the graph further on. As the graph shows, the per-capita health spending of nations is virtually independent of the age structure of its population.

Why, then, is the aging of the population such a small driver of annual increases in health spending? The answer can be found in the last graphical display of this commentary. That graph contains the same data as the first graph in this commentary, but the vertical axis is scaled as it should be scaled: from 0 percent to 100 percent. Letting it run from 12 percent to 22 percent stretches the vertical axis and creates the image of the famous Baby Boom Tsunami. It is a form of lying with statistics.

As this graph illustrates, the aging of our population is a very gradual process and does not come even close to resembling a tsunami. It is at best a demographic ripple.

Furthermore, current population projections have the fraction of elderly in the United States population peak at around 20 percent. Along with Canada and Australia, we shall be for a very long time the youngest nation in the O.E.C.D. Only in 2025 will the American population be as “old” as many European populations are already today.

As the song goes, relative to other nations we shall be “forever young”!

Uwe E. Reinhardt is an economist at Princeton.

Coverage mandate will fail as a health-care reform plan

By Rose Ann DeMoro

The Philadelphia Inquirer

Mon, Dec. 8, 2008

It’s time for Congress to stop getting carried away with financial bailouts for big industries, especially when it comes to some of the most-profitable and least-responsible companies: the health-insurance giants.

Two major trade lobbies, America’s Health Insurance Plans and the Blue Cross-Blue Shield Association, have announced that they would be willing to end their disgraceful practice of excluding people from coverage based on their health or age. In exchange, they want the federal government to force uninsured Americans to buy private insurance.

That would be exactly the wrong direction for health-care reform. Proposing mandatory coverage as the solution overlooks the one-fourth of insured Americans who are rationing their own medical care because they can’t afford to pay the bills. One in eight late-stage cancer patients turns down recommended care because of the cost, according to a recent report in USA Today.

And let’s not forget the insured patients who are denied needed treatments that their insurers don’t want to pay for.

A mandate for individuals turns the challenge of health-care reform on its head. It would be a massive bailout for one of the most merciless industries in America – and one that’s already rolling in cash. The 18 biggest insurers reported $16 billion in profit last year.

Now, in exchange for promising the coverage they should have provided all along, these insurers are demanding additional billions of dollars in profit from people who would face fines or other penalties if they didn’t hand over the cash.

The insurance giants’ proposal came in concert with one by Sen. Max Baucus (D., Mont.), the chairman of the influential Senate Finance Committee, who wants to make an individual mandate part of health-care reform. There is speculation that Sen. Ted Kennedy (D., Mass.), the other leading Senate voice on health-care reform, is considering including an individual mandate in whatever measure emerges from his Health, Education, Labor and Pensions Committee.

Mandatory coverage also was a component of Sen. Hillary Clinton’s health-care proposal when she sought the Democratic presidential nomination. Barack Obama wisely opposed the idea during the primaries.

A coverage mandate is the centerpiece of the Massachusetts health-care law that many see as Kennedy’s model. But the mandate is an unpopular disaster in Massachusetts; in California, public opposition to it helped kill a similar proposal.

Coupled with Massachusetts’ failure to rein in insurance price-gouging, the state’s mandate forces the typical middle-aged adult to spend more than $6,000 out of pocket on premiums and deductibles before medical expenses are covered.

No wonder the insurers like it. Tony Soprano would, too.

Ultimately, any reform plan that relies on such a mandate to establish “universal” coverage will fail.

Without restraints on skyrocketing insurance premiums and out-of-pocket costs, many families will face further economic distress, with little additional health security to show for it. And without tough regulatory oversight of insurers, patients will continue to endure inhumane denials of care.

The most effective way to fix our broken health-care system would look like Medicare, but improved and expanded to cover everyone. A single-payer, Medicare-for-all bill sponsored by Rep. John Conyers (D., Mich.) had more than 90 co-sponsors in the last Congress – more than any other reform bill. It is expected to be reintroduced early next year.

Such a program is the only way to control costs through negotiated fee schedules, global budgets, bulk purchasing, a huge cut in administrative waste, and other measures. And it’s the only way to wrest control of our health from the insurers.

Rose Ann DeMoro directs the California Nurses Association/ National Nurses Organizing Committee

For more information, see www.guaranteedhealthcare.org.

Private insurers and fairness of balance billing

Surprise Health Bills Make People See Red

By Anna Wilde Mathews

The Wall Street Journal

December 4, 2008

Insured patients are sometimes hit with unforeseen charges after emergencies, when they are taken to the closest hospital regardless of whether the facility accepts their insurance. Consumers also may be billed after visiting in-network hospitals if they received treatment from medical providers who work there but don’t participate in the same health plans. When that happens, insurers often pay part of the doctors’ fees, and the physicians bill patients for the difference. This is the practice known as balance billing, and it can leave consumers battling both the insurer and the medical provider to get the charge reduced.

California regulators recently made it illegal for people covered by health-maintenance organizations to be balance-billed for out-of-network emergency services.

Physician groups say doctors have the right to refuse to sign up with insurers’ networks, and regulators shouldn’t bar doctors who don’t participate in health plans from billing insured patients. They say that insurers’ payments to out-of-network health providers are often unfairly small. “You can’t turn it around and say it’s the doctor’s fault,” says Nancy Nielsen, president of the American Medical Association.

Insurers counter that they shouldn’t be forced to pay whatever fee out-of-network health-care providers demand. “You have a set of specialists who won’t contract with health plans, and they want to bill whatever they choose,” says Robert Zirkelbach, a spokesman for America’s Health Insurance Plans.

http://online.wsj.com/article/SB122834911902477643.html

Comment:

By Don McCanne, MD

Balance billing is a payment required by physicians that is in excess of the benefits covered by the patient’s insurer. It is a prime example of the unfairness that permeates our system of health care financing. It can be unfair for all parties.

Balance billing is certainly unfair for patients who purchased insurance in good faith only to find that they receive large bills for services that their insurance should have covered. Denying physicians the right to bill full fees for services that the patient’s insurer should have covered, but didn’t, is unfair to the physicians who have no contract with the insurer. Physicians who hold out for exorbitant fee schedules are unfair to the insurers who are trying to put together a reasonable list of in-network physicians to serve their beneficiaries.

Let’s step back and see if we can make some sense out of this.

Let’s agree that the goal of our health care financing system should be to be sure that everyone can receive the health care that they need without exposure to financial hardship. Not only are financial barriers removed for the patient, but also enough funds are allocated for the delivery system to be sure that it will be there when needed. Obviously that means that physicians should be adequately compensated.

Should physicians have the right to unilaterally dictate the fees that the third party payer must pay? When Medicare was introduced, we saw what happened. Fees skyrocketed. Medicare had to adopt payment policies that would ensure that compensation was reasonable. That has been and always will be a work in progress, but an effort continues to be made to provide a reasonable balance that would advance the public good: fair fees for physicians without an excess burden on taxpayers.

It is very rare to see balance billing for a patient enrolled in the traditional Medicare program (except maybe by error) since very few physicians totally opt out of the Medicare program. Those physicians who do not sign Medicare contracts are still required to adhere to a payment schedule unless they establish what amounts to a private contract with every Medicare patient they see.

What is the role of private insurers in setting fees? They establish a contract with patients to pay for services, but only under the terms of the contract. The only reason that private insurers still exist is that they also establish contracts with selected physicians and other providers who agree to the discounted reimbursement rates dictated by the insurer. Physicians who decline to sign contracts to become providers under these plans are free to charge any patient, whether or not covered by these plans, their usual fees. That is, until now.

California has made it illegal, in emergency situations, for physicians to bill the patient for balances not covered by the patient’s own insurance plan, even though the insurer has no contract with the physician. Think about that. The only contract is between the patient and the insurer, yet the state has given the insurer the authority to enforce upon physicians the terms of a contract that doesn’t even exist!

We’ve seen what’s unfair about balance billing, so how could we introduce fairness? If we had an improved Medicare program that covered everyone, the patient would never have to worry about being billed for balances that are not defined by the program. That’s fair. Under a universal Medicare program, reimbursement would be negotiated with physicians to be sure that rates were adequate to cover legitimate expenses and still provide reasonable profits. That’s fair.

And the private insurers who are extorting physicians with whom they have no contractual relationship, while they burn up resources on egregiously wasteful administrative excesses? With our own improved Medicare system we wouldn’t even need them, and we would show them the door. Now that’s really fair!

Health Reform via Guaranteed Choice

Examining Obama's health-care proposal

By Roger Bybee

Z Magazine

December, 01 2008

America’s health care system further unraveled relentlessly in 2008, with the Wall Street meltdown and economic uncertainty adding to citizens’ anxiety over their health care in an increasingly dicey future.

Barack Obama has put forward a plan that promises to avoid both government-run health care and the unregulated status quo dominated by big private insurers. Obama’s plan promises to allow Americans to keep their private insurance or enroll in a Medicare-style public plan, while imposing strong new regulations forcing insurers, for example, to accept enrollees without regard to pre-existing conditions.

The Obama plan is backed in its essentials by a new coalition called Health Care for America Now (HCAN) composed of labor and citizen-advocacy groups, which heralds its guaranteed choice proposal as “a bold new solution that gives you real choice and a guarantee of quality coverage you can afford: keep your current private insurance plan, pick a new private insurance plan, or join a public health insurance plan.”

But is the Obama-HCAN production destined to be a flop, a sequel to the failed 1993-94 Clinton health reform effort, which also left private insurance companies as the chief regulator of health care in America? Moreover, contrary to Obama’s statement that “health care is a right” during the final debate with John McCain (who labeled it a “responsibility”), the guaranteed choice approach overlooks the demise of state-based reforms heavily premised on individuals’ responsibility to purchase insurance for themselves and families. While the new effort features harsher rhetoric against insurers, it reinforces the illusion that the present system entitles individual consumers to freely pick their insurer, rather than the other way around. Guaranteed choice advocates also appear overconfident in the ability of regulators to force insurers to actually implement reforms.

Single-Payer Supporters & Detractors

Dr. Oliver Fein and Joanne Landy spotlight the central danger of the guaranteed choice strategy: “Halfway solutions won’t work, particularly those that put more taxpayer money into helping people buy more private health insurance. Private health insurance is not only extremely costly; it will also result in more and more under-insurance and actually moves us away from achieving universal health coverage. In order to maintain profits and control their costs, private insurers will jack up deductibles and co-pays and cut benefits, [while] do[ing] all they can to recruit the healthy and avoid the sick.”

Despite the structural flaws of Obama’s plan, his approach will at least allow progressives to argue that the public component of guaranteed choice should become the dominant model of U.S. health care reform.

Since George W. Bush’s became president in 2001, the deterioration of the health care system has proceeded exponentially. As a result, strong majorities of both the general public and doctors now favor a Canadian-style single-payer plan that would largely displace private insurers with one public authority in each state.

For example, in 2005, Business Week summarized its survey results among the public in these terms: “67 percent of all Americans think it’s a good idea to guarantee health care for all U.S. citizens, as Canada and Britain do, with just 27 percent dissenting.” More recently, a new poll published April 1 in the Annals of Internal Medicine shows that 59 percent of U.S. doctors support a “single-payer” plan that essentially dethrones private insurers. Moreover, Rep. John Conyers’s bill for single-payer health care, HR 676, has 92 co-signers, far more than any other health proposal in Congress.

Essentially, single-payer plans, operating in nations as diverse as Canada and Taiwan, provide health care to all citizens and permit them free choice of their doctors and hospitals. They also largely eliminate the commanding role of private insurers in the system and the huge administrative costs they impose, enabling the health system to cover every citizen. The single-payer plans are typically funded by a mixture of general tax revenues and payroll taxes.

However, the Obama-HCAN guaranteed choice policy direction would leave private insurers at the core of the health-care system, along with adding a public, Medicare-style option. Obama supports a model based upon an “individual mandate” to purchase private insurance. This mandate has been the shoal on which a number of state-level reform plans have crashed and splintered. Moreover, the guaranteed choice plan is premised on the illusion that individual consumers–rather than their employers or insurers–have the final say on insurance costs, coverage, and co-pays.

Further, the absence of effective cost controls in the guaranteed choice plan means that unrestrained medical cost inflation will undermine efforts to establish and retain coverage for all Americans. More and more ill and aging Americans will likely feel pressure to choose the public plan, leaving it with a disproportionately heavy burden of expensive patients gleefully abandoned by private insurers.

During the Democratic presidential primary, the effort to disqualify from serious consideration the single-payer alternative has been led by a group of influential public-interest and labor leaders, and academics who consider themselves realists, with almost the entire Democratic field of candidates following in their wake. These pragmatists–now gathered in HCAN–and are seeking to marginalize the single-payer approach in favor of guaranteed choice. The pragmatists insist that the American public is not fully committed to a publicly-administered insurance system and are now lobbying members of Congress with the argument that a single-payer plan is not viable. HCAN also includes a variety of groups including ACORN, Planned Parenthood, the SEIU, National Council of La Raza, and USAction.

Some of the pragmatists have not disguised their scorn for the single-payer approach. The SEIU’s Andrew Stern has proclaimed, “Americans want to have an American solution, not a Canadian solution.” In the same vein, Families USA’s Ron Pollack has stated that he favors an approach that “allow[s] a marketplace to [function] with some ground rules, as opposed to saying that government is going to make all the decisions”–a caricature of the single-payer plan that was employed in one Obama TV ad as noted above.

Clear Alternative Or Untested Plan?

In the eyes of single-payer advocates, the push for guaranteed choice threatens to fracture the potential unity behind a proven and comprehensible alternative, in favor of a much less coherent plan of questionable feasibility and limited ability to generate mass support. Don McCanne of the Physicians for a National Health Plan warns, “It is likely that the next president of the United States will enter office having campaigned on the promise of allowing you to keep the insurance you have”–a vow that will prove impossible to keep. “Keeping the insurance you have”–in terms of price, range of choices, and quality–is dependent on decisions made by employers and insurers, not employees, yet, “Large coalitions are forming to spread this gospel,” observes McCanne. “They are rejecting those who call for a national health plan [i.e., single-payer], stating that the policy debate is over, and now it is all about unity.”

The pragmatists’ call for a unified reform campaign rings somewhat hollow given the disparagement of the single-payer plan by prominent leaders like Pollack and Stern. Still, at least some of the pragmatists like Hickey, co-director of the Campaign for America’s Future, believe the public portion of the guaranteed coverage plan leaves enough room to accommodate both the single-payer and pragmatist wings behind it.

To justify their dismissing single-payer, the pragmatists contend that there is insufficient committed public support for such a system at this time. Hickey argues that polling shows that more than half of Americans like their present health care plan and are hesitant about plunging ahead into an entirely new system. He cites polling by the AFL-CIO, Stan Greenberg and his Democracy Corps, SEIU, Hart Research, Celinda Lake, and American Environics to back up his case.

Hickey said that the polling showed surprising strong support for the guaranteed choice approach, especially among African-American and Latino union members who seemingly feared that a public system would mean a second-class system, as is the case now with so many public institutions and programs. Among all groups, “We have picked up the attitude that a public program will be more like Medicaid than Medicare,” explains Hickey.

These various surveys illustrate that the single-payer plan is not immediately appealing even to those infuriated with the health system, Hickey says. Pollster Celinda Lake tested the guaranteed choice plan of tightly regulated private insurance for all against single-payer, and guaranteed choice “wins 64 percent support to 22 percent for single-payer,” Hickey reports. Further, he notes, “Even the hard core progressive part of the population, which Celinda [Lake] calls the ‘health justice’ constituency, favors guaranteed choice over single-payer.”

However, this finding seems to run directly counter to a CBS poll conducted September 14-16, 2007. The CBS survey found that 55 percent preferred “having one health insurance program covering all Americans that would be administered by the government and paid for by taxpayers,” compared with 29 percent who chose “keeping the current system where many people get their insurance from private employers and some have no insurance.”

Nonetheless, Hickey maintains that there is a widely-felt desire to hang on to existing insurance benefits, coupled with realism about corporate America’s relentless shrinkage of health care benefits. But there is little wonder why a majority would desperately hope, against a backdrop of fast-disappearing health benefits, to “keep the insurance you have.” “For healthier individuals who believe that they have good insurance, this concept polls very well. In fact, the other questions in the polls are now tailored to reinforce this simple concept,” McCanne points out.

The immediate health-care vista observed by most Americans is indeed frightening. U.S. corporations have been “remarkably successful at shifting health-care costs onto employees, their families, and other individuals,” notes Professor Marie Schalk–a success that also dampens corporate America’s self-interest in enacting health-care reform. Many employers are dropping coverage of their employees, skidding from about 75 percent in 1992-93 period to 64 percent in 2000 and then again falling to 60 percent in 2006. Similarly, many retirees, accustomed to employer plans supplementing Medicare, are finding that corporations are raising premiums astronomically or allocating a fixed sum for all retiree health costs, thereby placing the burden on workers or their unions.

Moreover, there is a well-grounded fear among the public that even “good” insurance coverage may instantly evaporate when an insurer faces paying for a costly treatment. Thus, the possibility of relying upon the “good insurance” side of the guaranteed choice plan seems like it is shrinking fast. Workers’ share of premiums is rising rapidly, far faster than wages, with the amount that workers pay toward family health-care coverage skyrocketing 87 percent since 2000.

Insurance Choices Generally Not Up To Workers

In this context, the polling by the guaranteed-choice advocates takes on a distinctly unreal air, say single-payer advocates. McCanne suggests a better survey question would be to ask: “When you did change coverage for reasons not really under your control, did the new plan have better benefits with lower costs than your prior plan?”

With employers flitting from one plan to another, sometimes on an annual basis, the notion of consistent, continuous health coverage has all but disappeared. “The average length of time a patient stays in any given private health insurance plan has dropped to less than two years,” notes Rose Anne DeMoro, director of the California Nurses Association. “Health insurance on a continual basis is practically non-existent in the private insurance market,” observes McCanne. In countless situations, “the insured individual was not granted the option of ‘keeping the insurance you have’,” McCanne notes.

While the pragmatists seem eager to close down policy debate and plunge ahead with a campaign for their “winnable” guaranteed choice plan, there is a need to thoroughly examine a number of unanswered questions about the proposal. Even if enacted relatively intact–despite the best efforts of the insurers and their allies–Obama’s guaranteed choice plan would likely encounter very serious problems for four reasons:

(1) Bad drives out the good. One immediate barrier to guaranteed choice working is “adverse selection,” with private insurers–even under new constraints about accepting all applicants–using a variety of subtle techniques to drive older and sicker patients into the public program. For example, private insurers might use the denial of authorization for treatments to drive away more costly patients. The existing laws and regulatory bodies can do little to effectively protect patients from such unfair denials of care, as insurers routinely use pretexts like “cost cutting” or “quality control” to justify their actions.

As Dr. Steffie Woolhandler puts it, “If you have two groups trying to enroll people in health plans, the bad guys will drive the good guys out of business. The bad guys will selectively recruit healthier people, and push sicker people onto the single-payer plan. Competition is not something that works with health care.”

This could even trigger what McCanne calls a “death spiral” for the public plan. “The competition will not be fair because the private insurers will figure how to attract the well by offering perks like free health-club memberships and by advertising aggressively among healthier groups,” write Landy and Fein. “Even if they are legally required to insure all applicants,” insurers have already shown a high degree of sophistication in carefully marketing to attract the healthy and avoid those with significant health problems. “This will inevitably leave a disproportionate number of the sick to Medicare, which will in turn raise Medicare premiums, which will make it less attractive to healthy people than private insurance,” Landy and Fein predict.

Meanwhile, private insurers will continue to try to use their political clout to “game the system,” securing unfair subsidies like the 12 to 19 percent in extra payments to insurers offering Medicare Advantage programs.

(2) The savings that would accrue from slashing administrative costs are sacrificed. Clearly, retaining the for-profit insurers forsakes almost all of the potential $350 billion to $400 billion a year in excess administrative overhead that could be eliminated by a single-payer system. Private insurers with their huge overhead costs devoted to a strategy of “denial management”–i.e., paying as few claims as possible–would remain in operation. At the same time, providers would need to maintain their own huge clerical apparatus to fight to minimize the rejection rate of the insurers. Thus, even with a parallel public system attracting a substantial number of patients, most of the overhead costs would still remain as insurers would maintain their bureaucracies and providers such as hospitals and doctors being forced to cope with multiple insurers with intricate differences in coverage.

(3) Meaningful cost controls are absent. The guaranteed choice plan also lacks an effective brake on the greed of for-profit insurers and their ability to boost profits by continually raising premiums. Notably, the guaranteed choice plan remains weak on keeping insurers from further raising premiums purportedly in return for taking on what they view as distasteful and unprofitable obligations. Though the guaranteed choice plan would require insurers to accept all applicants (a practice known as guaranteed issue), insurers may sabotage these regulations via large premium increases and by refusing to authorize needed treatments. Potentially, insurers could also be forced to swallow regulation of their “loss ratio”–the ratio of funds devoted to providing patient care to the enormous funds absorbed in executive pay, profits, marketing, and their massive administrative overhead. But it would take an army of government regulators to guard against insurers improperly allocating all kinds of administrative costs as medical expenses for anything that can be labeled as an effort to improve quality and cut costs.

The cost-cutting mechanisms produced thus far by guaranteed choice advocates fall far short of the proven effectiveness of the single-payer plan in holding down costs through the elimination of bureaucracy and a role for the public in negotiating prices with hospitals, doctors, and pharmaceutical firms. In comparison, Canada’s per-person health costs are about half of costs in the U.S. ($3,326 per person in Canada vs. $6,697 in the U.S).

From the single-payer side, Woolhandler of Harvard Medical School and a co-founder of Physicians for a National Health Plan, says, “There’s not another plan that will work. All of the other proposals lack feasibility in terms of economics. The other plans simply won’t get you to universal health care. The key to the economic feasibility of the single payer plan is administrative savings.” Only by realizing those savings–by replacing the private insurers with state-level governmental bodies coupled with negotiated prices with providers–can a system of universal care actually be sustained.

(4) Individual mandates are unaffordable. The backers of guaranteed choice see a mandate for individuals buying health insurance as essential for assuring universal coverage. But these mandates have universally failed, as is occurring now with the new Massachusetts Connector Plan, as Woolhandler pointed out: “The fundamental assumption is that the uninsured have enough money to buy insurance policies that they can buy their way out of the predicament. If they had the money, they’d already have insurance. They don’t have money in the first place. Someone my age, in their 50s, and making over $29,400 a year, would get no subsidy. The cost of that premium would be $4,200 a year, but along with that there’s a $2,000 deductible before any coverage begins, co-pays, and co-insurance after that first $2,000.”

The result is that hundreds of thousands of residents are unable to afford insurance, even if they face stiff financial penalties for failure to enroll. Numerous state-level “universal” plans have sunk upon the very same rock in Massachusetts, Oregon, Tennessee, Minnesota, Vermont, and Washington.

Essentially, plans requiring an individual mandate have been configured to prevent a necessary showdown with private health insurers and their unaffordable premiums. As Woolhandler and Himmelstein observe, “The mandate model for health care rests on impeccable political logic: avoiding challenging insurance firms’ stranglehold on health care. But it is economic nonsense. The reliance on private insurers makes universal coverage unaffordable.”

The outcome is “coverage without care,” as Dr. Marcia Angell puts it. This ultimately has a corrosive effect on the public’s confidence in government’s ability to serve their interests, much as the defeat of Clinton’s complex and insurer-centered health-care plan did in 1994. As economist Robert Kuttner puts it, “Universal social insurance signals government help. A mandate signals government coercion.” Such an approach seems destined to waste the massive support for a single-payer health system.

Despite Barack Obama’s avowed hopes for change, a guaranteed choice plan, manacled to private insurers, may ultimately deepen public cynicism about the possibility of any substantive help with their increasingly desperate health care situation.

Roger Bybee is a Milwaukee-based activist and writer. His articles have appeared in numerous publications.

Does AHIP have a plan for us!

Now is the Time for Health Care Reform: A Proposal to Achieve Universal Coverage, Affordability, Quality Improvement and Market Reform

AHIP (America’s Health Insurance Plans)

Board of Directors’ Statement

December 2008

… the Board of Directors of America’s Health Insurance Plans (AHIP) is offering a new set of proposals aimed at moving the nation toward a restructured health care system in which no one falls through the cracks, all Americans have high quality, affordable coverage, and the efficiency and effectiveness of the system are greatly improved.

Soaring Health Care Costs Need To Be Brought Under Control

3. Streamline administrative processes to increase efficiency, make the system easier for patients and providers to navigate, and reduce costs.

Administrative processes should be streamlined across the health care system. In advancing this recommendation, we recognize the need for our industry to come to the table with proposals for how we can do our part. We have committed to develop a multi-payer online portal to give providers a uniform method to communicate with health plans and afford them access to current information on eligibility and benefits. This will ease the administrative challenges that physicians and other providers face, and will help them and their patients better understand coverage and predict out-of-pocket costs. We are also working with providers on a standard data aggregation approach with the goal of giving providers and consumers useful performance information. Administrative streamlining should be viewed through the eyes of consumers, with the goal of making the health care system easier to navigate and more consumer friendly. A key part of this effort is our focus on the reform of market rules to enhance access for consumers and provide them with clear, useable information on coverage and care options.

http://www.americanhealthsolution.org/assets/Uploads/healthcarereformproposal.pdf

Comment:

By Don McCanne, MD

As the momentum for reform builds in our nation’s capitol, the board of directors of AHIP has made the wise decision to provide a definitive statement of their concepts of reform. Very soon the future role of their industry in the financing of health care in America may well be defined by political policy makers. Obviously the industry wants policies that will ensure a robust market for their products.

Although there are many important concepts presented in their report, only the statement on administrative efficiency was selected for this message. The reason is that the private insurance industry has been a major contributor to the profound administrative waste that characterizes our dysfunctional, fragmented system of financing health care. If the private insurers are to have a legitimate role in the future of our health care system, the first requirement that we should demand of them is administrative efficiency.

Reading their proposal to “streamline administrative processes,” you have to ask yourself, what is the substance of their proposal? They are recommending a continuation of the same inefficient, fragmented structure that we now have, except that it is expanded to include everyone. Their call for a token online portal will not provide the structural reform that we need, and may actually increase the administrative burden of our financing system. The fact that they have failed to seriously address this administrative waste, largely of their own making, in and of itself should disqualify them from further participation in the reform process.

This is not to say that this report has no redeeming value. There are some worthwhile proposals. They have stressed the importance of improving our primary care infrastructure. They also have recommended an expansion of our public health infrastructure. These are much needed investments that have been neglected far too long. But the last thing that we would want to do is to superimpose private insurer administrative functions on these crucial programs. The report states “health plans are uniquely positioned to assist in this effort,” but what we need is for the insurance industry to get out of our way as we introduce these repairs to our health care delivery system.

If you still believe that the private insurers have a legitimate role in health care financing, all you need to do is read the relatively detailed section on insurance markets, public programs, and regulation. You could not possibly describe a proposal that would better serve the interests of the private insurance industry. They would create a standard of underinsurance, require all of us to purchase their products, and pretend to address affordability issues through tax credits. The private insurance industry wins the jackpot, while patients and taxpayers lose.

The AHIP board of directors must feel quite smug in having foisted off on us this con job. But wait. This is only their vision; it is not yet our reality. We can do something. We can demand reform that benefits patients and taxpayers. Do you think Washington can hear us?

Insurance industry positions itself for the fight ahead

By CHRIS FRATES

Politico

12/3/08

With President-elect Barack Obama showing no signs of backing off his pledge to push health care reform early in his administration, jockeying is intensifying among interest groups to position themselves for the fight ahead.

The latest to step forward: the health insurance industry.

America’s Health Insurance Plans, the industry trade group, rolled out a plan Wednesday that embraces some of Obama’s ideas and signals dissent with others.

The industry’s proposal would require individuals to carry insurance and insurers to cover pre-existing conditions. And it would strengthen the health care safety net and provide tax credits to working families to help buy insurance.

The insurers say their plan would build on the employer-based system that provides most Americans with their health insurance — also an idea Obama supports.

What it doesn’t include is a public health insurance option that would compete with private plans, a concept supported by Obama and progressive groups such as Health Care for America Now.

“We don’t see that there will be a need for an additional public option. We don’t think there will be a need to get the government in the insurance business,” said the group’s spokesman, Michael Tuffin.

The industry has begun shopping its plan on Capitol Hill, paying particular attention to the Senate, where Health Committee Chairman Sen. Edward M. Kennedy (D-Mass.) and Senate Finance Committee Chairman Max Baucus (D-Mont.) are working on legislative proposals. It also began building a grassroots army that they can mobilize when legislation starts moving.

“The insurance industry has advanced serious proposals that deserve serious analysis and consideration,” said Kennedy spokesman Anthony Coley.

But Health Care for America Now said the insurance industry’s proposal doesn’t make insurance more affordable. For instance, it doesn’t prevent companies from charging sick and elderly beneficiaries more.

“What they’re trying to do politically is to get ahead of health care reform and shape health care reform in such a way to protect their bottom line as opposed to actually fixing the problems in the health care system,” said the group’s national campaign manager, Richard Kirsch.

He criticized the industry’s plan to prevent medical bankruptcy by providing tax credits to low-income families that would cap total health care expenses instead of offering more affordable plans — a move that Kirsch put this way: “We’ll continue to let you go bankrupt, and we’ll have the government bail you out.”

The industry addresses the affordability issue by calling on Congress to reduce health care costs by 30 percent.

The nation’s largest nurses union has an idea for how to cut those costs: eliminate the insurance industry and switch to a single-payer system. About 30 percent of the system’s cost is from insurance company profits and administration costs, said Rose Ann DeMoro, executive director of the California Nurses Association/National Nurses Organizing Committee.

“It’s the Marshall Plan for insurance industry profits, because they use all the arms of government to force people to buy their failed product,” she said. “What their proposal does is privatize profits and socialize risk.”

Doctors oppose US health plan

By Rebecca Knight in Boston

Financial Times

Published: August 4 2008

The Massachusetts healthcare programme widely seen as a test case for universal health coverage in the US faces mounting opposition from doctors who say the reform is failing.

More than 250 physicians in the state have signed an open letter warning that the healthcare plan, which was signed into law in April 2006 by Mitt Romney, the former Republican governor of Massachusetts, is “already proving fiscally unsustainable”.

The landmark programme, designed to provide uniÂversal health insurance, requires all uninsured people to purchase private insurance or face a fine or tax penalty.

The doctors’ discontent with the plan, and their support for a single-payer system — whereby payments to healthcare providers would all be made by one administrative body like Britain’s National Health Service, rather than individual insurers — could send a strong signal to other states considering similar reform measures.

Healthcare is one of the main issues on the presidential campaign trail. Both candidates have called for radical reform of the $2,300bn (€1,477bn, £1,172bn ) healthcare system, although neither supports mandatory insurance payments.

In the letter, the Massachusetts doctors say the state-subsidised insurance offered to low-income families is too expensive and that “few can afford premiums for even the skimpiest coverage”. The doctors also warn that funding the plan in future will be hard because it deepened the state’s “dependence on private insurance, [so] can only add coverage by adding costs”.

The Massachusetts plan is an example of “the same reform being tried over and over”, according to Dr Rachel Nardin, assistant professor of neurology at Harvard Medical School, who wrote the letter. “This kind of incremental reform is very popular because it’s politically feasible: it allows the current stakeholders to stay in play,” she said. “But there are a lot reasons why it can’t work.”

A growing number of US doctors favour switching to a national healthcare plan. According to an earlier survey in the journal Annals of Internal Medicine, 59 per cent of doctors said they backed legislation to establish a national health insurance programme, a rise of 10 per cent from 2002.

Copyright The Financial Times Limited 2008