By Claudia Fegan, M.D.

Common Dreams, Jan. 1, 2025

How should we react when a man is shot to death on the street on his way to work? Our humanity tells us that we should be shocked and horrified—and feel that something is deeply wrong with such a brazen act of murder. Ideally, we would do what we could to help sooth the survivors, condemn the violence, and bring the perpetrator to justice.

So why did hundreds of thousands of people have the exact opposite reaction when UnitedHealthcare CEO Brian Thompson was executed in New York City last month? Because Americans are furious with health insurance corporations—and they have every right to be.

In the immediate aftermath of the shooting, many Americans took to social media not to mourn, but to celebrate. Caustic posts about prior authorization and denied medical claims were common. Sympathetic statements were met with rancor—and in the case of UnitedHealth Group’s own statement, over 70,000 “laugh reactions” before the company made that tally private. Even verbose political figures like Elon Musk and President-elect Donald Trump declined to comment for days. This shooting touched a raw nerve.

As a physician who’s treated countless victims of gun violence, and who’s life’s work is to care for all of my patients, I found this response to be deeply unnerving. But I also can’t waive it away with simple explanations like online radicalization or trolling. Something much deeper is at play.

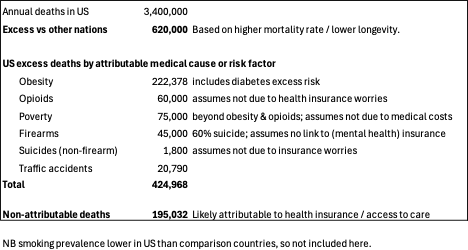

For decades, health insurance corporations like United have been growing more powerful and more profitable. How do they generate these profits? By taking in as much money as possible in premiums and paying out as little as possible in medical claims. Over time, they have tried everything from requiring “prior authorization” of care, to excluding high-quality providers from their networks, to imposing a Byzantine series of charges including ever-growing copays, coinsurance, and deductibles. When all else fails, many insurers simply deny claims.

Behind each of these practices are millions of Americans who are made to suffer. I hear these stories routinely in my practice, and they never become easier to stomach. I have seen patients with aggressive cancer who avoided seeing a doctor for months because they feared bankruptcy; patients with chronic conditions like diabetes who are denied treatments that would improve their quality of life; and gunshot victims whose fight to recover and gain a semblance of normalcy is complicated by their health plans saying no, no, and no again.

I have seen patients suffer and die in order to pad the bottom lines of corporate health insurers—and in recent years I have seen this problem getting much worse.

These are the stories that Americans are sharing in this fraught moment. We have to ask ourselves: Are we listening? And what are we going to do about it?

Insurers like UnitedHealthcare will have their own responses. Their PR teams will no doubt work overtime to marginalize aggrieved voices and to highlight what they consider to be the “value” of their health plans. Expect to see glossy commercials and towering billboards touting the “peace of mind” that Americans should enjoy knowing that their medical needs are “covered.” But the health insurance industry doesn’t have a communications problem, it has a profiteering problem—and no amount of marketing will convince people who have already been burned.

Behind the scenes, corporate insurers will no doubt lobby for the preferential treatment they have come to expect. Our newly elected Congress may acquiesce, or they may decide that the industry needs to be regulated—a strategy that has failed to live up to its promise.

Republicans and Democrats have made separate attempts to combine federal requirements with federal largesse in order to make corporate health insurers play nice. But both the Affordable Care Act and the Medicare Advantage program have only succeeded in ballooning the profits of firms like United—without improving Americans’ health or sparing their wallets.

It’s also clear that violence is not the answer, both on a purely human level and because corporate insurers will simply not be moved. UnitedHealthcare will have a new CEO in short order, and it will be that person’s responsibility to boost profits and make shareholders wealthier. Responding to patients’ cries will not serve these ends, so it is not in the cards.

What would help is a proven reform proposal that is long overdue: a single-payer national health program. Such a system would provide universal coverage and comprehensive benefits—with zero out-of-pocket costs. It could be easily implemented given the gargantuan sums we spend on healthcare in this country, and it would be a boon for those who are suffering, and for those who are fearful.

Americans are crying out in pain—and are recognizing that they are not alone in their pain. We should listen to these cries and we should finally, after decades of delay, do something about it.