By Uwe E. Reinhardt

New York Times

December 19, 2008

Uwe E. Reinhardt is an economist at Princeton. For previous posts in his series on why America pays so much for health care, click here, here, here and here.

It is now generally believed that the federal Medicare program for America’s elderly is “unsustainable” and must be “restructured.” This somber assessment is part of the more general cri de coeur so wondrously phrased some years ago in the title of the Brookings Institution’s monograph “Can America Afford to Grow Old?”

What if we couldn’t? What would we do — push the elderly into the ocean on an ice floe?

Of course America can afford to grow old! We can more easily afford it than most other industrialized nations.

The percentage of the American population age 65 or over is 12.4 now and is projected to rise to about 21 by 2050. Only 7 percent of China’s population is 65 or over now, but that figure will shoot up rapidly to over 22 percent by 2050. And in a number of other industrialized countries — notably in Japan, Germany, Italy and Sweden — the elderly already represent close to 20 percent of the population, a level the United States will not reach until about 2040. Yet the world has not come to an end in these older countries.

It’s hard to say what fraction of America’s gross domestic product future generations should allocate to people too old (or too young) to work, and how much should remain with those who have produced that G.D.P. This is a matter to be resolved by those future generations.

They must decide how well the elderly in their midst should be housed, fed and cared for when sick. Our influence over that allocation is minimal, because future generations can always override our decisions while we cannot override theirs. The best we can do today is to put in place public policies that can help G.D.P. grow now and in the future, to ease the pain of sharing. We could also influence somewhat the age structure of future populations through current and future policies on immigration, although there are limits to that approach, because immigrants, too, grow old.

Fortunately, as is shown in the graphical display below, future generations will most likely have the benefit of G.D.P. growth on their side, which should make it easier for them to house, feed and care for a larger fractions of elderly citizens.

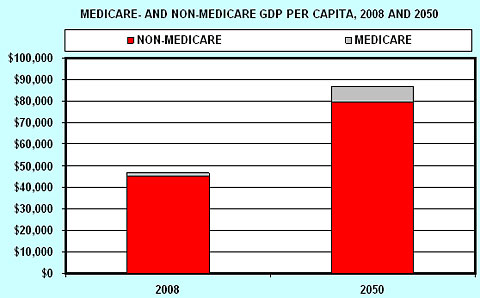

Current G.D.P. per capita in the United States is about $46,500 (tables B-2 and B-34 here), of which Medicare absorbs slightly over 3 percent, leaving about $45,000 of G.D.P. per capita for other things.

Suppose between now and, say, 2050, inflation-adjusted G.D.P. per capita in the United States grows at an annual compound rate of only 1.5 percent per year, which is conservatively below the roughly 2 percent long-run annual growth rate of real G.D.P. per capita over the past several decades. Even at this low growth rate, inflation-adjusted G.D.P. per capita would grow from $46,500 now to about $87,000 by 2050.

According to the Social Security Trustees’ 2008 Report on the Status of the Social Security and Medicare Programs (Chart B), Medicare will absorb about 8.4 percent of G.D.P. by 2050 if it is not restructured.

But even after that 8.4 percent haircut for Medicare in 2050, there would still be close to $80,000 inflation-adjusted G.D.P. per capita left over for other things in that year, which is still 78 percent more than the non-Medicare G.D.P. per capita than we have today.

So what do we mean when we lament that Medicare will not be “affordable” in the future? Do we assume that G.D.P. will be stagnant for the next 40 years?

Those who make such statements, of course, may not even think about real claims on real G.D.P. Instead they may have in mind two quite different propositions.

First, they may argue that even if Medicare were eminently affordable from a purely macroeconomic perspective, its current structure of mainly public financing may not be politically sustainable. There is no question that to allocate as much as 8.4 percent of 2050 G.D.P. to Medicare under its current structure would require sizable tax increases. But social values and preferences can change. Future cohorts of voting retirees and their children in the United States may well countenance the higher levels of taxation already long accepted in other industrialized nations, in return for greater personal financial security.

An alternative proposition may be that, even if (1) sustaining Medicare in its current structure were eminently affordable from a macroeconomic perspective, and (2) it were politically feasible, we still shouldn’t sustain Medicare in its present form because the program wastes real and financial resources.

There is something to the second proposition, as will be explained in detail in my next post to this blog.