http://www.boston.com/bostonglobe/editorial_opinion/dan_wasserman_cartoonist/

Uwe Reinhardt on whether community rating is fair

Is ‘Community Rating’ in Health Insurance Fair?

By Uwe E. Reinhardt

The New York Times, Economix

January 1, 2010

One controversial feature of the health reform bill winding its way through Congress is “community rating.” The term has a mellow ring but is apt to be divisive.

“Community rating” refers to the practice of charging a common premium to all members of a heterogeneous risk pool who may have widely varied health spending for the year. It inevitably makes chronically healthy individuals subsidize with their insurance premiums (rather than through overt taxes and transfers) the health care used by chronically sicker individuals.

The purpose of any insurance, of course, is to do precisely that: redistribute the financial burden from the unlucky to the lucky members of a risk pool.

(Professor Reinhardt then provides calculations for an example of two cohorts, A and B, representing populations segregated into two pools with different risks, as is characteristic of our price-competitive market for individually sold health insurance.)

Would it be “fair” that the healthy individuals of cohort A pay a pure insurance premium of only $2,450 a year, while the sicker citizens in cohort B must pay $6,600? This is, after all, how health insurance now is priced in most states for individuals.

Or does “fairness” require that the two groups be merged into one large national risk pool A & B, whose risk profile is shown in the right-most column of the table. If each member of this merged pool is to pay the same pure premium, then the latter will have to be $4,525 to break even. Such a premium would be said to be “community rated” over these two distinct risk pools.

Relative to their premium in a perfectly risk-segregated market, the community-rated premium of $4,525 will cost members of low-risk cohort A $2,075 more and the sicker members of cohort B $2,075 less than they would have paid in a risk-segregated market. Is that “fair”?

So what should the political leaders of this imaginary country do? It would be interesting to have your reaction. It is, after all, the very question our political leaders are tackling this moment.

Should you choose to respond, would you indicate your age?

(You can post a response by clicking on “Post a Comment” at the end of the full article at the following link. You can also recommend specific responses.)

http://economix.blogs.nytimes.com/2010/01/01/is-community-rating-in-health-insurance-fair/

Posted response of Don McCanne, San Juan Capistrano, CA (response # 9):

One of the more obvious examples of this dilemma is the disagreement as to the premiums that should be charged for the healthier population in their twenties as opposed to the less healthy population, on average, in their fifties and early sixties. Congress has already decided that strict community rating through a single premium for everyone will not apply to age differences, but they remain conflicted as to how much of a transfer will occur from the younger healthier individuals to the older less healthy individuals. They seem to believe that the concept of such a transfer is “fair,” but they are not in agreement as to what level of transfer exceeds their concept of fairness.

My wife and I are in our seventies and benefit from Medicare, a program in which there is a transfer to us from those in their twenties, many of whom are uninsured. Is that fair?

Of course the issue is further complicated by our nation’s very high health care costs since there is a need to transfer from the wealthy to lower income individuals, if, in fact, we agree that we should have a financing system that allows everyone to have the essential health care that they need. The many other complexities introduced by our fragmented health financing system, using public and private sources, complicates the process of finding the right premium for the right coverage, for the right amount of cost sharing, with the right amount of subsidies to support the premiums and the cost sharing.

With our unique health financing system already overburdened with profound administrative waste, it doesn’t seem rational to try to expand coverage by assigning inevitably inequitable premiums to benefit packages within fragmented private plan risk pools. That just adds to the complexities, inequities and administrative waste.

It would be much more efficient and equitable to remove the risk bearing function from the private insurers, thereby eliminating premiums, and replace our dysfunctional health care financing system with a single universal risk pool covering everyone. Each person would pay into the pool their fair share, based on ability to pay, by funding it through progressive taxes.

This could easily be accomplished through an improved Medicare for all. But some may not consider this fair either if they reject the concept of social solidarity, the concept on which community rating is based.

Health care 'overhaul'? The devil's in the details

By Andrew Coates

Rochester City Newspaper

December 29, 2009

As health insurance reform inches towards the president’s desk, the airwaves and editorial pages fill with spin. “Health-care overhaul,” the headlines say. “Still a government takeover of health care,” the Republicans in Congress say. “The culmination of a struggle begun by Theodore Roosevelt,” Vice President Biden says.

Against so much political posturing, Representative Eric Massa has proven himself unique in Congress: someone who sticks to the facts. Last month when he courageously voted against the House bill, he said it would strengthen, not weaken, the hand of the private insurers. The insurance industry is the problem, not the solution, he explained. As the legislation nears final reconciliation, Massa’s analysis remains solid.

The crux of the legislation in Congress is compulsory private insurance. Under the “individual mandate,” a long-held wish of the insurance companies, the government will coerce people to become and remain their paying customers.

If you’re uninsured and you don’t buy health insurance, the Senate bill allows a fine of up to 2 percent of your income, assessed by the IRS. (It’s 2.5 percent in the House bill.) Pay the fine and you’re free to remain uninsured.

If you simply can’t afford a policy, according to the Senate bill, you can avoid paying the fine by applying for a “hardship waiver.” Get the waiver and you’re free to remain uninsured.

Since the legislation does nothing to make insurance affordable, tax money will subsidize private insurance premiums for those who earn up to 400 percent of the federal poverty level. But those earning up to 400 percent of the poverty level would still have to pay up to 9.8 percent of their income for insurance (under the Senate bill). This taxpayer gift to insurance companies will amount to as much as $476 billion – half a trillion dollars – over a decade.

The Senate formula also pushes the onus of health costs onto individual families by imposing a 40 percent tax on high-cost health plans, an incentive to reduce coverage. This will especially impact residents of states with high insurance costs, like our own state; union members with comprehensive benefits; companies that employ women (whose group insurance costs are higher), and plans that cover older employees (whose insurance costs are higher).

The Senate bill also encourages skimpy coverage by allowing the most basic plans to cover only 60 percent of actual health costs on top of growing of out-of-pocket expenses. Prescription drug costs have gone up 9 percent this year. Meanwhile, the insurance industry itself has estimated premium hikes of 79 to 111 percent over the coming decade.

In addition to millions of new customers for insurance companies, the legislation seeks an enormous expansion of Medicaid, with new enrollment of millions of people by expanding eligibility to those who earn up to 150 percent of the federal poverty level. But we know from bitter experience that having Medicaid is no guarantee of access to care, nor will it reduce disparities in care.

If private insurance will remain a defective product and Medicaid will remain a poor program for poor people and the legislation will not reign in costs – where is the reform?

But perhaps most startling is that the major features of the legislation would not begin until 2013, after the next presidential election, and then would take effect gradually over six years more. Such a proposal hardly seems worthy of the name “overhaul” when we remember that Medicare passed in 1965 and was up and running in 1966.

Last month when he voted against the House bill, Congressman Massa explained that he had studied the entire bill and that he understood the health care needs of his district. As the Congressional process lumbers forth, with the pending legislation ever more insurance-industry-friendly, Eric Massa has emerged as a portrait of leadership, courage, and honesty.

It’s time to scrap this pro-insurance-company legislation and start over. A good starting point would be the improvement and expansion of Medicare to cover every person in the United States.

Andrew Coates practices medicine in Albany, where he is assistant professor of medicine and psychiatry at AlbanyMedicalCollege. He is a member of the board of directors of Physicians for a National Health Program.

Health care ‘overhaul’? The devil’s in the details

By Andrew Coates

Rochester City Newspaper

December 29, 2009

As health insurance reform inches towards the president’s desk, the airwaves and editorial pages fill with spin. “Health-care overhaul,” the headlines say. “Still a government takeover of health care,” the Republicans in Congress say. “The culmination of a struggle begun by Theodore Roosevelt,” Vice President Biden says.

Against so much political posturing, Representative Eric Massa has proven himself unique in Congress: someone who sticks to the facts. Last month when he courageously voted against the House bill, he said it would strengthen, not weaken, the hand of the private insurers. The insurance industry is the problem, not the solution, he explained. As the legislation nears final reconciliation, Massa’s analysis remains solid.

The crux of the legislation in Congress is compulsory private insurance. Under the “individual mandate,” a long-held wish of the insurance companies, the government will coerce people to become and remain their paying customers.

If you’re uninsured and you don’t buy health insurance, the Senate bill allows a fine of up to 2 percent of your income, assessed by the IRS. (It’s 2.5 percent in the House bill.) Pay the fine and you’re free to remain uninsured.

If you simply can’t afford a policy, according to the Senate bill, you can avoid paying the fine by applying for a “hardship waiver.” Get the waiver and you’re free to remain uninsured.

Since the legislation does nothing to make insurance affordable, tax money will subsidize private insurance premiums for those who earn up to 400 percent of the federal poverty level. But those earning up to 400 percent of the poverty level would still have to pay up to 9.8 percent of their income for insurance (under the Senate bill). This taxpayer gift to insurance companies will amount to as much as $476 billion – half a trillion dollars – over a decade.

The Senate formula also pushes the onus of health costs onto individual families by imposing a 40 percent tax on high-cost health plans, an incentive to reduce coverage. This will especially impact residents of states with high insurance costs, like our own state; union members with comprehensive benefits; companies that employ women (whose group insurance costs are higher), and plans that cover older employees (whose insurance costs are higher).

The Senate bill also encourages skimpy coverage by allowing the most basic plans to cover only 60 percent of actual health costs on top of growing of out-of-pocket expenses. Prescription drug costs have gone up 9 percent this year. Meanwhile, the insurance industry itself has estimated premium hikes of 79 to 111 percent over the coming decade.

In addition to millions of new customers for insurance companies, the legislation seeks an enormous expansion of Medicaid, with new enrollment of millions of people by expanding eligibility to those who earn up to 150 percent of the federal poverty level. But we know from bitter experience that having Medicaid is no guarantee of access to care, nor will it reduce disparities in care.

If private insurance will remain a defective product and Medicaid will remain a poor program for poor people and the legislation will not reign in costs – where is the reform?

But perhaps most startling is that the major features of the legislation would not begin until 2013, after the next presidential election, and then would take effect gradually over six years more. Such a proposal hardly seems worthy of the name “overhaul” when we remember that Medicare passed in 1965 and was up and running in 1966.

Last month when he voted against the House bill, Congressman Massa explained that he had studied the entire bill and that he understood the health care needs of his district. As the Congressional process lumbers forth, with the pending legislation ever more insurance-industry-friendly, Eric Massa has emerged as a portrait of leadership, courage, and honesty.

It’s time to scrap this pro-insurance-company legislation and start over. A good starting point would be the improvement and expansion of Medicare to cover every person in the United States.

Andrew Coates practices medicine in Albany, where he is assistant professor of medicine and psychiatry at AlbanyMedicalCollege. He is a member of the board of directors of Physicians for a National Health Program.

Uwe Reinhardt on whether community rating is fair

Is ‘Community Rating’ in Health Insurance Fair?

By Uwe E. Reinhardt

The New York Times, Economix

January 1, 2010

One controversial feature of the health reform bill winding its way through Congress is “community rating.” The term has a mellow ring but is apt to be divisive.

“Community rating” refers to the practice of charging a common premium to all members of a heterogeneous risk pool who may have widely varied health spending for the year. It inevitably makes chronically healthy individuals subsidize with their insurance premiums (rather than through overt taxes and transfers) the health care used by chronically sicker individuals.

The purpose of any insurance, of course, is to do precisely that: redistribute the financial burden from the unlucky to the lucky members of a risk pool.

(Professor Reinhardt then provides calculations for an example of two cohorts, A and B, representing populations segregated into two pools with different risks, as is characteristic of our price-competitive market for individually sold health insurance.)

Would it be “fair” that the healthy individuals of cohort A pay a pure insurance premium of only $2,450 a year, while the sicker citizens in cohort B must pay $6,600? This is, after all, how health insurance now is priced in most states for individuals.

Or does “fairness” require that the two groups be merged into one large national risk pool A & B, whose risk profile is shown in the right-most column of the table. If each member of this merged pool is to pay the same pure premium, then the latter will have to be $4,525 to break even. Such a premium would be said to be “community rated” over these two distinct risk pools.

Relative to their premium in a perfectly risk-segregated market, the community-rated premium of $4,525 will cost members of low-risk cohort A $2,075 more and the sicker members of cohort B $2,075 less than they would have paid in a risk-segregated market. Is that “fair”?

So what should the political leaders of this imaginary country do? It would be interesting to have your reaction. It is, after all, the very question our political leaders are tackling this moment.

Should you choose to respond, would you indicate your age?

(You can post a response by clicking on “Post a Comment” at the end of the full article at the following link. You can also recommend specific responses.)

http://economix.blogs.nytimes.com/2010/01/01/is-community-rating-in-health-insurance-fair/

Posted response of Don McCanne, San Juan Capistrano, CA (response # 9):

One of the more obvious examples of this dilemma is the disagreement as to the premiums that should be charged for the healthier population in their twenties as opposed to the less healthy population, on average, in their fifties and early sixties. Congress has already decided that strict community rating through a single premium for everyone will not apply to age differences, but they remain conflicted as to how much of a transfer will occur from the younger healthier individuals to the older less healthy individuals. They seem to believe that the concept of such a transfer is “fair,” but they are not in agreement as to what level of transfer exceeds their concept of fairness.

My wife and I are in our seventies and benefit from Medicare, a program in which there is a transfer to us from those in their twenties, many of whom are uninsured. Is that fair?

Of course the issue is further complicated by our nation’s very high health care costs since there is a need to transfer from the wealthy to lower income individuals, if, in fact, we agree that we should have a financing system that allows everyone to have the essential health care that they need. The many other complexities introduced by our fragmented health financing system, using public and private sources, complicates the process of finding the right premium for the right coverage, for the right amount of cost sharing, with the right amount of subsidies to support the premiums and the cost sharing.

With our unique health financing system already overburdened with profound administrative waste, it doesn’t seem rational to try to expand coverage by assigning inevitably inequitable premiums to benefit packages within fragmented private plan risk pools. That just adds to the complexities, inequities and administrative waste.

It would be much more efficient and equitable to remove the risk bearing function from the private insurers, thereby eliminating premiums, and replace our dysfunctional health care financing system with a single universal risk pool covering everyone. Each person would pay into the pool their fair share, based on ability to pay, by funding it through progressive taxes.

This could easily be accomplished through an improved Medicare for all. But some may not consider this fair either if they reject the concept of social solidarity, the concept on which community rating is based.

The New York Times doesn't get it

This editorial from today’s edition of The New York Times makes their case for supporting the current health reform legislation before Congress. The responses of Don McCanne, MD are in red and bracketed with ***.

The Case for Reform

Editorial

The New York Times

December 29, 2009

Reforming this country’s broken health care system is an urgent and essential task.

*** Absolutely! ***

Given all of the fabrications and distortions from Republican critics, and the squabbling among Democratic supporters, it is no surprise that many Americans still have doubts.

*** Unfortunately, the Republicans are handicapped by their ideological opposition to government solutions for social problems. Their proposal for a free market of cheap underinsurance products sold across state lines would only make problems worse by further impairing the effectiveness of our current inadequate and inequitable risk pools. The squabbling of the Democrats is based on a disagreement over whether to take the bold step of providing a truly effective universal public insurance program, such as an improved Medicare for everyone, or to take what some believe to be the politically expedient step of trying to modify our current dysfunctional system, even though it means falling far short of the goals of universality and affordability. ***

President Obama and Democratic leaders have a strong case. They need to make it now.

*** They have a very weak case. President Obama and the Democratic leadership chose to try to modify our current dysfunctional system, leaving tens of millions without insurance and perpetuating the financial hardships faced by many who need health care. ***

Here are compelling reasons for all Americans to root for the reform effort to succeed and urge Congress to complete the job:

THE HEALTH OF MILLIONS OF AMERICANS

The fact that 46 million people in this country have no health insurance should be intolerable. Every other major industrial country guarantees health coverage to its citizens, yet the United States, the richest of them all, does not.

*** The current proposal would leave close to 20 million people without insurance, a number that is destined to increase as health care costs continue to rise. Supporting a policy that ensures that so many will continue to be without health insurance is what should not be tolerated. A public insurance program is designed to automatically cover everyone. ***

Claims that the uninsured can always go to an emergency room for charity care ignore the fact that American taxpayers pay a high price for that care. And it ignores the abundant evidence that people who lack insurance don’t get necessary preventive care or screening tests, and suffer gravely when they finally do seek treatment because their diseases have become critical.

*** The modest marginal cost of providing care for additional patients in the emergency room is not a major issue. The crucial problem is the deterioration of our primary care infrastructure that is required to provide individuals with a source of seamless continuing care. The proposed legislation does take some important steps toward addressing this serious deficiency, but they would be much more effective with a single, unified financing system integrated with our health care delivery system. ***

The American Cancer Society now says the greatest obstacle to reducing cancer deaths is lack of health insurance. It is so persuaded of that fact that two years ago, instead of promoting its antismoking campaign or publicizing the need for cancer screening, it devoted its entire advertising budget to the problem of inadequate health insurance coverage.

*** We previously commended the American Cancer Society for taking this forward-thinking position. ***

We consider it a moral obligation and sound policy to provide health insurance to as many people as possible. While the pending bills would fall short of complete coverage, by 2019, the Senate bill would cover 31 million people and the House bill 36 million who would otherwise be uninsured under current trends.

*** It is both a moral obligation and sound policy to provide health insurance for everyone, which a universal public insurance program would do. The design of the current proposal is both immoral and unsound because it leaves an intolerable number of individuals uninsured – a number close to two-thirds of the population of Canada. We may criticize Canada’s queues, but we would be outraged if they prohibited two-thirds of their population from even having a place in the queues. Why is there no outrage here when we would leave a similar number without coverage? ***

MORE SECURITY FOR ALL

Horror stories abound of people — mainly those who buy individual policies — who were charged exorbitant premiums or rejected because of pre-existing conditions or paid out for years and then had their policies rescinded when they got sick.

Such practices would be prohibited completely in three or four years under the reform bills. Before that, insurers would be barred from rescinding policies retroactively and the bills would establish temporary high-risk pools to cover people with pre-existing conditions.

*** Although private insurers have been appropriately condemned for using trivial reasons to rescind policies, many rescissions were for the legitimate reason (legitimate in a business sense) that individuals who were uninsured and then developed serious problems purchased coverage without reporting their newly acquired problem – a form of fraud. That defeats the insurance function of pooling all of the healthy in with the sick. The proposal before Congress still permits rescissions for fraud. This problem would totally disappear in a public financing system in which enrollment for life is automatic. Also, the experience with high-risk pools to date has been very dismal. The need for high-risk pools would be eliminated by a single public universal risk pool. ***

The legislation would also allow unmarried dependent children to remain on their parents’ policies until age 26 (the Senate version) or age 27 (the House version).

*** What do they do at 26 or 27? Would everyone at that age have a great job with generous employer-sponsored benefits? If not, would they be eligible for plans in the exchange, and could they afford their portion of premiums and out-of-pocket expenses that is estimated to be about 20 percent of their income? Again, this problem would disappear in an equitably-financed public program in which everyone is automatically enrolled for life. ***

If reform legislation is approved, employees enrolled in group coverage at work would also be more secure. If workers are laid off — an all too common occurrence these days — and need to buy policies on their own, insurers would be barred from denying them coverage or charging exorbitant premiums for health reasons.

*** Just like COBRA, laid-off employees who no longer have a paycheck must then pay the full insurance premium that was formerly heavily subsidized by their employers. Partial subsidies are not adequate for a person with no paycheck. Even if eligible for the backup of Medicaid, shifting in and out of programs is disruptive to care. ***

CUTTING COSTS

Americans are justifiably concerned about the rising cost of health insurance and of the medical care it covers. The reform bills won’t solve these problems quick

ly, but they would make a good start.

*** The reform bills do not solve the problem of rising costs, and they don’t even make a good start. The proposals for accountable care organizations and bundling of payments create nightmare logistical problems that are dismissed as something we can figure out later. The excise tax on higher-premium plans will result in diminished benefits, shifting more of the financial responsibility to those individuals who need care and are already burdened with excessive out-of-pocket expenses. As health care costs continue to increase, more plans will be pared of benefits in order to avoid the excise tax. Making essential health care less affordable is a perverse policy proposal. Strengthening the power of an independent MedPAC-like board to reduce spending only within the Medicare program threatens to diminish the support of those in the health care delivery system who already feel threatened by what they perceive to be already low reimbursement rates. Price discrimination is a major problem in our dysfunctional financing system, but it cannot be adequately addressed by a payment advisory board limited to Medicare. Although the current proposal would look at the private sector, it would have no power nor even the ability to slow cost increases in the private sector. Under a universal public financing program, the board would be able to recommend measures to improve resource allocation for our entire health care delivery system, while balancing the demands of patients, health care providers and taxpayers. ***

Despite overheated Republican claims that the reforms would drive up premiums, the Congressional Budget Office projected that under the Senate bill the vast majority of Americans (those covered by employer policies) would see little or no change in their average premiums or even a slight decline. Those who buy their own policies would pay somewhat more — but for greatly improved coverage.

*** Except for a few regulatory requirements for the insurance industry, most Americans will see no improvement. They will continue to be burdened with ever higher health care costs, reflected in higher premiums and greater out-of-pocket cost sharing. Being guaranteed the right to buy insurance is of little consolation for those who can’t pay for it. Those in the individual market are often uninsured because they can’t afford the stripped-down plans currently available. Requiring greater benefits makes these plans even less affordable. The inadequacy of the proposed subsidies which are limited to plans purchased through the exchange will provide little consolation for those who are not eligible for or who cannot afford the plans in the exchange. A universal public system equitably financed based on ability to pay would eliminate the need for individual or employer-sponsored private plans. ***

Most people who would be buying their own policies would qualify for tax subsidies to help pay their premiums, which could reduce their costs by thousands of dollars a year. And small businesses would qualify for tax credits to defray the cost of covering their workers.

*** The primary reason to propose tax subsidies is to keep the insurance industry alive. It is much less efficient than establishing a single universal risk pool financed by equitable taxes. Furthermore, the proposed subsidies would leave all but the wealthiest of us exposed to a potential obligation to pay about 20 percent of our incomes for health care. That is a burden that most would find very difficult to bear. ***

The inexorably rising cost of hospital and medical care is the underlying factor that drives up premiums, deductibles and co-payments. No one yet has an answer to the problem.

*** Balderdash! All sane economists agree that a single payer monopsony would solve the problem. Conservative economists might not like a government solution, but they agree that it would actually work. It’s time for the practitioners of the dismal science of economics to engage in normative economics. These are not only numbers we’re dealing with; they are about the lives and well being of people. ***

But the bills would launch an array of pilot projects to test new payment and health care delivery systems within Medicare. These include, for example, incentives to coordinate hospital and post-hospital care to head off needless readmissions, better coordination of care for the chronically ill, and incentives for doctors to provide a patient’s total care for a flat fee instead of charging for each test or service provided.

*** Continual improvement in health care delivery is an important goal, but it is in no way unique to the current legislative proposal. A single payer monopsony would have a greater capability of realigning incentives for optimal care. ***

The Senate bill would set up an independent board to spur the use of programs that save money or improve care — subject to Congressional veto. Optimists believe the savings might come quickly but this could still take many years. Without passing a reform bill, there is little chance of success.

*** See the first comment under “cutting costs.” ***

THE TIME HAS COME

For decades, presidents from both parties have tried in vain to reform the health care system and cover the uninsured. Still many Americans wonder, given the deep recession, whether it makes sense to do it now. The first thing to keep in mind is that the C.B.O. says that the reform bills are paid for over the next 10 years and would actually reduce future deficits.

The need is clear and the political timing is right with the Democrats controlling the White House, the Senate and the House. If this chance is squandered and Republicans gain seats, as expected, in the midterm elections, it could be a decade or more before reformers have another opportunity. Americans shouldn’t have to wait any longer.

*** Most of the major features of this legislation are not scheduled to begin for years, yet we are told that it is urgent that we pass this bill within the next several weeks. The urgency is not based on sound health policy but is based on the political goal of proving President Obama and the Democrats with a political victory well in advance of the next elections. That might be good politics, but it is an unforgivable neglect of duty that is being committed by our public stewards. The policies of a single payer Medicare for all program are much less complex than the dysfunctional model being foisted off on us with the misnomer of reform. Because of the toll of financial hardship, physical suffering and even death, there is urgency in the need to act. But we can act now and have the program fully up and running long before the dates proposed in the current legislation. The New York Times says that we are squabbling, by definition arguing about trivial matters. Racking up a political victory on the scorecard is trivial. Doing that while glibly accepting a system that will leave so many broke and uninsured is unconscionable. ***

NYT editorial, The Case for Reform: http://www.nytimes.com/2009/12/30/opinion/30wed2.html

The New York Times doesn’t get it

This editorial from today’s edition of The New York Times makes their case for supporting the current health reform legislation before Congress. The responses of Don McCanne, MD are in red and bracketed with ***.

The Case for Reform

Editorial

The New York Times

December 29, 2009

Reforming this country’s broken health care system is an urgent and essential task.

*** Absolutely! ***

Given all of the fabrications and distortions from Republican critics, and the squabbling among Democratic supporters, it is no surprise that many Americans still have doubts.

*** Unfortunately, the Republicans are handicapped by their ideological opposition to government solutions for social problems. Their proposal for a free market of cheap underinsurance products sold across state lines would only make problems worse by further impairing the effectiveness of our current inadequate and inequitable risk pools. The squabbling of the Democrats is based on a disagreement over whether to take the bold step of providing a truly effective universal public insurance program, such as an improved Medicare for everyone, or to take what some believe to be the politically expedient step of trying to modify our current dysfunctional system, even though it means falling far short of the goals of universality and affordability. ***

President Obama and Democratic leaders have a strong case. They need to make it now.

*** They have a very weak case. President Obama and the Democratic leadership chose to try to modify our current dysfunctional system, leaving tens of millions without insurance and perpetuating the financial hardships faced by many who need health care. ***

Here are compelling reasons for all Americans to root for the reform effort to succeed and urge Congress to complete the job:

THE HEALTH OF MILLIONS OF AMERICANS

The fact that 46 million people in this country have no health insurance should be intolerable. Every other major industrial country guarantees health coverage to its citizens, yet the United States, the richest of them all, does not.

*** The current proposal would leave close to 20 million people without insurance, a number that is destined to increase as health care costs continue to rise. Supporting a policy that ensures that so many will continue to be without health insurance is what should not be tolerated. A public insurance program is designed to automatically cover everyone. ***

Claims that the uninsured can always go to an emergency room for charity care ignore the fact that American taxpayers pay a high price for that care. And it ignores the abundant evidence that people who lack insurance don’t get necessary preventive care or screening tests, and suffer gravely when they finally do seek treatment because their diseases have become critical.

*** The modest marginal cost of providing care for additional patients in the emergency room is not a major issue. The crucial problem is the deterioration of our primary care infrastructure that is required to provide individuals with a source of seamless continuing care. The proposed legislation does take some important steps toward addressing this serious deficiency, but they would be much more effective with a single, unified financing system integrated with our health care delivery system. ***

The American Cancer Society now says the greatest obstacle to reducing cancer deaths is lack of health insurance. It is so persuaded of that fact that two years ago, instead of promoting its antismoking campaign or publicizing the need for cancer screening, it devoted its entire advertising budget to the problem of inadequate health insurance coverage.

*** We previously commended the American Cancer Society for taking this forward-thinking position. ***

We consider it a moral obligation and sound policy to provide health insurance to as many people as possible. While the pending bills would fall short of complete coverage, by 2019, the Senate bill would cover 31 million people and the House bill 36 million who would otherwise be uninsured under current trends.

*** It is both a moral obligation and sound policy to provide health insurance for everyone, which a universal public insurance program would do. The design of the current proposal is both immoral and unsound because it leaves an intolerable number of individuals uninsured – a number close to two-thirds of the population of Canada. We may criticize Canada’s queues, but we would be outraged if they prohibited two-thirds of their population from even having a place in the queues. Why is there no outrage here when we would leave a similar number without coverage? ***

MORE SECURITY FOR ALL

Horror stories abound of people — mainly those who buy individual policies — who were charged exorbitant premiums or rejected because of pre-existing conditions or paid out for years and then had their policies rescinded when they got sick.

Such practices would be prohibited completely in three or four years under the reform bills. Before that, insurers would be barred from rescinding policies retroactively and the bills would establish temporary high-risk pools to cover people with pre-existing conditions.

*** Although private insurers have been appropriately condemned for using trivial reasons to rescind policies, many rescissions were for the legitimate reason (legitimate in a business sense) that individuals who were uninsured and then developed serious problems purchased coverage without reporting their newly acquired problem – a form of fraud. That defeats the insurance function of pooling all of the healthy in with the sick. The proposal before Congress still permits rescissions for fraud. This problem would totally disappear in a public financing system in which enrollment for life is automatic. Also, the experience with high-risk pools to date has been very dismal. The need for high-risk pools would be eliminated by a single public universal risk pool. ***

The legislation would also allow unmarried dependent children to remain on their parents’ policies until age 26 (the Senate version) or age 27 (the House version).

*** What do they do at 26 or 27? Would everyone at that age have a great job with generous employer-sponsored benefits? If not, would they be eligible for plans in the exchange, and could they afford their portion of premiums and out-of-pocket expenses that is estimated to be about 20 percent of their income? Again, this problem would disappear in an equitably-financed public program in which everyone is automatically enrolled for life. ***

If reform legislation is approved, employees enrolled in group coverage at work would also be more secure. If workers are laid off — an all too common occurrence these days — and need to buy policies on their own, insurers would be barred from denying them coverage or charging exorbitant premiums for health reasons.

*** Just like COBRA, laid-off employees who no longer have a paycheck must then pay the full insurance premium that was formerly heavily subsidized by their employers. Partial subsidies are not adequate for a person with no paycheck. Even if eligible for the backup of Medicaid, shifting in and out of programs is disruptive to care. ***

CUTTING COSTS

Americans are justifiably concerned about the rising cost of health insurance and of the medical care it covers. The reform bills won’t solve these problems quickly, but they would make a good start.

*** The reform bills do not solve the problem of rising costs, and they don’t even make a good start. The proposals for accountable care organizations and bundling of payments create nightmare logistical problems that are dismissed as something we can figure out later. The excise tax on higher-premium plans will result in diminished benefits, shifting more of the financial responsibility to those individuals who need care and are already burdened with excessive out-of-pocket expenses. As health care costs continue to increase, more plans will be pared of benefits in order to avoid the excise tax. Making essential health care less affordable is a perverse policy proposal. Strengthening the power of an independent MedPAC-like board to reduce spending only within the Medicare program threatens to diminish the support of those in the health care delivery system who already feel threatened by what they perceive to be already low reimbursement rates. Price discrimination is a major problem in our dysfunctional financing system, but it cannot be adequately addressed by a payment advisory board limited to Medicare. Although the current proposal would look at the private sector, it would have no power nor even the ability to slow cost increases in the private sector. Under a universal public financing program, the board would be able to recommend measures to improve resource allocation for our entire health care delivery system, while balancing the demands of patients, health care providers and taxpayers. ***

Despite overheated Republican claims that the reforms would drive up premiums, the Congressional Budget Office projected that under the Senate bill the vast majority of Americans (those covered by employer policies) would see little or no change in their average premiums or even a slight decline. Those who buy their own policies would pay somewhat more — but for greatly improved coverage.

*** Except for a few regulatory requirements for the insurance industry, most Americans will see no improvement. They will continue to be burdened with ever higher health care costs, reflected in higher premiums and greater out-of-pocket cost sharing. Being guaranteed the right to buy insurance is of little consolation for those who can’t pay for it. Those in the individual market are often uninsured because they can’t afford the stripped-down plans currently available. Requiring greater benefits makes these plans even less affordable. The inadequacy of the proposed subsidies which are limited to plans purchased through the exchange will provide little consolation for those who are not eligible for or who cannot afford the plans in the exchange. A universal public system equitably financed based on ability to pay would eliminate the need for individual or employer-sponsored private plans. ***

Most people who would be buying their own policies would qualify for tax subsidies to help pay their premiums, which could reduce their costs by thousands of dollars a year. And small businesses would qualify for tax credits to defray the cost of covering their workers.

*** The primary reason to propose tax subsidies is to keep the insurance industry alive. It is much less efficient than establishing a single universal risk pool financed by equitable taxes. Furthermore, the proposed subsidies would leave all but the wealthiest of us exposed to a potential obligation to pay about 20 percent of our incomes for health care. That is a burden that most would find very difficult to bear. ***

The inexorably rising cost of hospital and medical care is the underlying factor that drives up premiums, deductibles and co-payments. No one yet has an answer to the problem.

*** Balderdash! All sane economists agree that a single payer monopsony would solve the problem. Conservative economists might not like a government solution, but they agree that it would actually work. It’s time for the practitioners of the dismal science of economics to engage in normative economics. These are not only numbers we’re dealing with; they are about the lives and well being of people. ***

But the bills would launch an array of pilot projects to test new payment and health care delivery systems within Medicare. These include, for example, incentives to coordinate hospital and post-hospital care to head off needless readmissions, better coordination of care for the chronically ill, and incentives for doctors to provide a patient’s total care for a flat fee instead of charging for each test or service provided.

*** Continual improvement in health care delivery is an important goal, but it is in no way unique to the current legislative proposal. A single payer monopsony would have a greater capability of realigning incentives for optimal care. ***

The Senate bill would set up an independent board to spur the use of programs that save money or improve care — subject to Congressional veto. Optimists believe the savings might come quickly but this could still take many years. Without passing a reform bill, there is little chance of success.

*** See the first comment under “cutting costs.” ***

THE TIME HAS COME

For decades, presidents from both parties have tried in vain to reform the health care system and cover the uninsured. Still many Americans wonder, given the deep recession, whether it makes sense to do it now. The first thing to keep in mind is that the C.B.O. says that the reform bills are paid for over the next 10 years and would actually reduce future deficits.

The need is clear and the political timing is right with the Democrats controlling the White House, the Senate and the House. If this chance is squandered and Republicans gain seats, as expected, in the midterm elections, it could be a decade or more before reformers have another opportunity. Americans shouldn’t have to wait any longer.

*** Most of the major features of this legislation are not scheduled to begin for years, yet we are told that it is urgent that we pass this bill within the next several weeks. The urgency is not based on sound health policy but is based on the political goal of proving President Obama and the Democrats with a political victory well in advance of the next elections. That might be good politics, but it is an unforgivable neglect of duty that is being committed by our public stewards. The policies of a single payer Medicare for all program are much less complex than the dysfunctional model being foisted off on us with the misnomer of reform. Because of the toll of financial hardship, physical suffering and even death, there is urgency in the need to act. But we can act now and have the program fully up and running long before the dates proposed in the current legislation. The New York Times says that we are squabbling, by definition arguing about trivial matters. Racking up a political victory on the scorecard is trivial. Doing that while glibly accepting a system that will leave so many broke and uninsured is unconscionable. ***

NYT editorial, The Case for Reform: http://www.nytimes.com/2009/12/30/opinion/30wed2.html

Hold the Hyperbole on the Senate Health Bill

By Matthew Rothschild

The Progressive

December 24, 2009

Hold the champagne.

And don’t get rolled over by the hyperbole.

The Senate health care bill, which just passed 60-39, is nothing to cheer about.

It will do “more harm than good,” say the leaders of Physicians for a National Health Program.

They acknowledge “the salutary provisions included in the legislation, notably an expansion of Medicaid coverage, increased funds for community clinics, and regulations to curtail some of private insurers’ most egregious practices,” write Dr. Oliver Fein, Dr. David Himmelstein, and Dr. Steffie Woolhandler.

But these are outweighed, they say, by the bill’s killer flaws.

The individual mandate “would reinforce private insurers’ stranglehold on care” by forcing millions of people to buy insurance on the private market. “Those who dislike their current employer-sponsored coverage would be forced to keep it,” they write. “Those without insurance would be forced to pay private insurers’ inflated premiums, often for coverage so skimpy that serious illness would bankrupt them.”

The individual mandate, by the way, was the top priority of the private insurance lobby.

The leaders of the single-payer organization cite four other problems with the bill.

One: “The bill’s anti-abortion provisions would restrict reproductive choice, compromising the health of women and adolescent girls.”

Two: “The new 40 percent tax on high-cost health plans—deceptively labeled a ‘Cadillac tax’—would hit many middle-income families.”

Three: “The bill would drain $43 billion from Medicare payments to safety-net hospitals, threatening the care of the 23 million who will remain uninsured even if the bill works as planned.”

And four: “The bill would leave hundreds of millions of Americans with inadequate insurance. . . . Predictably, as health care costs continue to grow, more families will face co-payments and deductibles so high that they preclude adequate access to care.”

This last point puts the lie to the claim that the bill will cover 26 million more Americans. Actually, it will force most of those 26 million either to buy private insurance or pay a fine of $750 a person or $2,250 a family by the year 2016. Millions of people will likely to choose to pay that fine rather than pay the premiums, co-pays, and deductibles that can reach four, five, or six times the fine.

National Nurses United, the newly formed union of 150,000 nurses, also opposes the bill.

It points out that the much-heralded prohibition on not covering people with preexisting conditions is far less than meets the eye.

For instance, “insurers can charge four times more based on age plus more for certain conditions, and continue to use marketing techniques to cherry-pick healthier, less costly enrollees. So the insurance companies might not have a policy of not covering preexisting conditions, but they would have a practice of doing it.

Also, check this out: “Insurers may continue to rescind policies for ‘fraud or intentional misrepresentation’—the main pretext insurance companies now use to cancel coverage,” notes the nurses’ union.

Much of the bill is a straight up handout to the private insurance companies.

Remember the Medicare buy in proposal for people between the ages of 55 and 65? Well, that’s gone from the bill, and in its place, the government will pay employers and the insurance companies for covering the part of this cohort that is retired. The program “will reimburse employers or insurers for 80 percent of retiree claims between $15,000 and $90,000,” the bill says, according to an excellent breakdown by the Kaiser Family Foundation.

Gone, too, of course, is any public option.

“Sadly, we have ended up with legislation that fails to meet the true test of health care reform, guaranteeing high quality, cost-effective care for all Americans,” said Karen Higgins, co-president of National Nurses United. Instead, she added, we are “further locking into place a system that entrenches the chokehold of the profit-making insurance giants on our health.”

No wonder the stocks of those giants are soaring.

http://www.progressive.org/wx122409.html

Graph: The Cost of Care

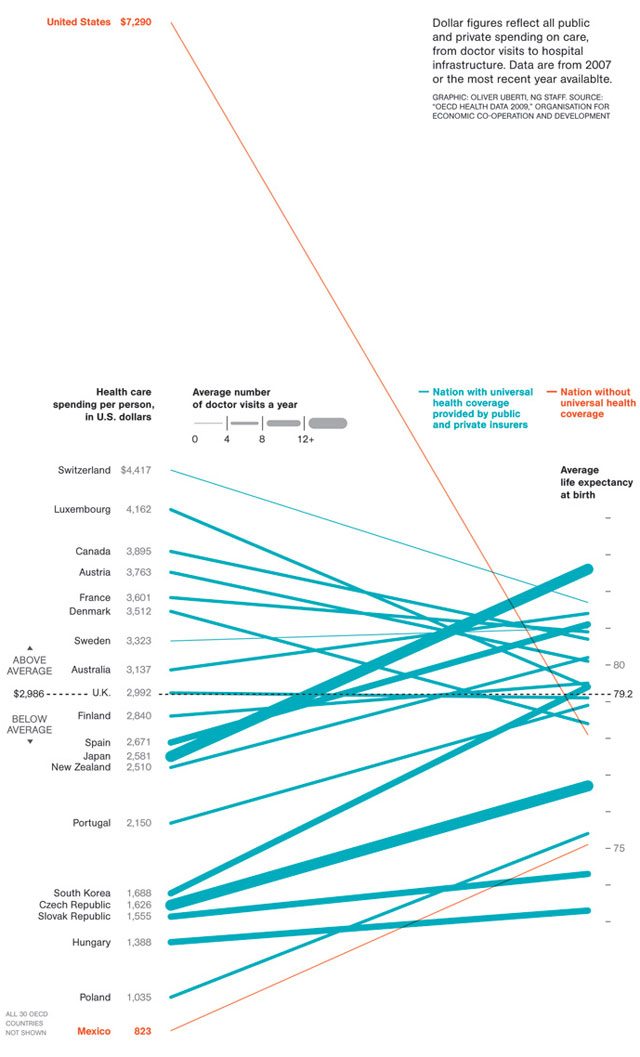

By Michelle Andrews

National Geographic Blog

Posted Dec 18, 2009

The United States spends more on medical care per person than any country, yet life expectancy is shorter than in most other developed nations and many developing ones. Lack of health insurance is a factor in life span and contributes to an estimated 45,000 deaths a year. Why the high cost? The U.S. has a fee-for-service system—paying medical providers piecemeal for appointments, surgery, and the like. That can lead to unneeded treatment that doesn’t reliably improve a patient’s health. Says Gerard Anderson, a professor at Johns Hopkins Bloomberg School of Public Health who studies health insurance worldwide, “More care does not necessarily mean better care.”

http://blogs.ngm.com/blog_central/2009/12/the-cost-of-care.html

The New York Times doesn't get it

This editorial from today’s edition of The New York Times makes their case for supporting the current health reform legislation before Congress. The responses of Don McCanne, MD are in red and bracketed with ***.

The Case for Reform

Editorial

The New York Times

December 29, 2009

Reforming this country’s broken health care system is an urgent and essential task.

*** Absolutely! ***

Given all of the fabrications and distortions from Republican critics, and the squabbling among Democratic supporters, it is no surprise that many Americans still have doubts.

*** Unfortunately, the Republicans are handicapped by their ideological opposition to government solutions for social problems. Their proposal for a free market of cheap underinsurance products sold across state lines would only make problems worse by further impairing the effectiveness of our current inadequate and inequitable risk pools. The squabbling of the Democrats is based on a disagreement over whether to take the bold step of providing a truly effective universal public insurance program, such as an improved Medicare for everyone, or to take what some believe to be the politically expedient step of trying to modify our current dysfunctional system, even though it means falling far short of the goals of universality and affordability. ***

President Obama and Democratic leaders have a strong case. They need to make it now.

*** They have a very weak case. President Obama and the Democratic leadership chose to try to modify our current dysfunctional system, leaving tens of millions without insurance and perpetuating the financial hardships faced by many who need health care. ***

Here are compelling reasons for all Americans to root for the reform effort to succeed and urge Congress to complete the job:

THE HEALTH OF MILLIONS OF AMERICANS

The fact that 46 million people in this country have no health insurance should be intolerable. Every other major industrial country guarantees health coverage to its citizens, yet the United States, the richest of them all, does not.

*** The current proposal would leave close to 20 million people without insurance, a number that is destined to increase as health care costs continue to rise. Supporting a policy that ensures that so many will continue to be without health insurance is what should not be tolerated. A public insurance program is designed to automatically cover everyone. ***

Claims that the uninsured can always go to an emergency room for charity care ignore the fact that American taxpayers pay a high price for that care. And it ignores the abundant evidence that people who lack insurance don’t get necessary preventive care or screening tests, and suffer gravely when they finally do seek treatment because their diseases have become critical.

*** The modest marginal cost of providing care for additional patients in the emergency room is not a major issue. The crucial problem is the deterioration of our primary care infrastructure that is required to provide individuals with a source of seamless continuing care. The proposed legislation does take some important steps toward addressing this serious deficiency, but they would be much more effective with a single, unified financing system integrated with our health care delivery system. ***

The American Cancer Society now says the greatest obstacle to reducing cancer deaths is lack of health insurance. It is so persuaded of that fact that two years ago, instead of promoting its antismoking campaign or publicizing the need for cancer screening, it devoted its entire advertising budget to the problem of inadequate health insurance coverage.

*** We previously commended the American Cancer Society for taking this forward-thinking position. ***

We consider it a moral obligation and sound policy to provide health insurance to as many people as possible. While the pending bills would fall short of complete coverage, by 2019, the Senate bill would cover 31 million people and the House bill 36 million who would otherwise be uninsured under current trends.

*** It is both a moral obligation and sound policy to provide health insurance for everyone, which a universal public insurance program would do. The design of the current proposal is both immoral and unsound because it leaves an intolerable number of individuals uninsured – a number close to two-thirds of the population of Canada. We may criticize Canada’s queues, but we would be outraged if they prohibited two-thirds of their population from even having a place in the queues. Why is there no outrage here when we would leave a similar number without coverage? ***

MORE SECURITY FOR ALL

Horror stories abound of people — mainly those who buy individual policies — who were charged exorbitant premiums or rejected because of pre-existing conditions or paid out for years and then had their policies rescinded when they got sick.

Such practices would be prohibited completely in three or four years under the reform bills. Before that, insurers would be barred from rescinding policies retroactively and the bills would establish temporary high-risk pools to cover people with pre-existing conditions.

*** Although private insurers have been appropriately condemned for using trivial reasons to rescind policies, many rescissions were for the legitimate reason (legitimate in a business sense) that individuals who were uninsured and then developed serious problems purchased coverage without reporting their newly acquired problem – a form of fraud. That defeats the insurance function of pooling all of the healthy in with the sick. The proposal before Congress still permits rescissions for fraud. This problem would totally disappear in a public financing system in which enrollment for life is automatic. Also, the experience with high-risk pools to date has been very dismal. The need for high-risk pools would be eliminated by a single public universal risk pool. ***

The legislation would also allow unmarried dependent children to remain on their parents’ policies until age 26 (the Senate version) or age 27 (the House version).

*** What do they do at 26 or 27? Would everyone at that age have a great job with generous employer-sponsored benefits? If not, would they be eligible for plans in the exchange, and could they afford their portion of premiums and out-of-pocket expenses that is estimated to be about 20 percent of their income? Again, this problem would disappear in an equitably-financed public program in which everyone is automatically enrolled for life. ***

If reform legislation is approved, employees enrolled in group coverage at work would also be more secure. If workers are laid off — an all too common occurrence these days — and need to buy policies on their own, insurers would be barred from denying them coverage or charging exorbitant premiums for health reasons.

*** Just like COBRA, laid-off employees who no longer have a paycheck must then pay the full insurance premium that was formerly heavily subsidized by their employers. Partial subsidies are not adequate for a person with no paycheck. Even if eligible for the backup of Medicaid, shifting in and out of programs is disruptive to care. ***

CUTTING COSTS

Americans are justifiably concerned about the rising cost of health insurance and of the medical care it covers. The reform bills won’t solve these problems quickly, but they would make a good start.

*** The reform bills do not solve the problem of rising costs, and they don’t even make a good start. The proposals for accountable care organizations and bundling of payments create nightmare logistical problems that are dismissed as something we can figure out later. The excise tax on higher-premium plans will result in diminished benefits, shifting more of the financial responsibility to those individuals who need care and are already burdened with excessive out-of-pocket expenses. As health care costs continue to increase, more plans will be pared of benefits in order to avoid the excise tax. Making essential health care less affordable is a perverse policy proposal. Strengthening the power of an independent MedPAC-like board to reduce spending only within the Medicare program threatens to diminish the support of those in the health care delivery system who already feel threatened by what they perceive to be already low reimbursement rates. Price discrimination is a major problem in our dysfunctional financing system, but it cannot be adequately addressed by a payment advisory board limited to Medicare. Although the current proposal would look at the private sector, it would have no power nor even the ability to slow cost increases in the private sector. Under a universal public financing program, the board would be able to recommend measures to improve resource allocation for our entire health care delivery system, while balancing the demands of patients, health care providers and taxpayers. ***

Despite overheated Republican claims that the reforms would drive up premiums, the Congressional Budget Office projected that under the Senate bill the vast majority of Americans (those covered by employer policies) would see little or no change in their average premiums or even a slight decline. Those who buy their own policies would pay somewhat more — but for greatly improved coverage.

*** Except for a few regulatory requirements for the insurance industry, most Americans will see no improvement. They will continue to be burdened with ever higher health care costs, reflected in higher premiums and greater out-of-pocket cost sharing. Being guaranteed the right to buy insurance is of little consolation for those who can’t pay for it. Those in the individual market are often uninsured because they can’t afford the stripped-down plans currently available. Requiring greater benefits makes these plans even less affordable. The inadequacy of the proposed subsidies which are limited to plans purchased through the exchange will provide little consolation for those who are not eligible for or who cannot afford the plans in the exchange. A universal public system equitably financed based on ability to pay would eliminate the need for individual or employer-sponsored private plans. ***

Most people who would be buying their own policies would qualify for tax subsidies to help pay their premiums, which could reduce their costs by thousands of dollars a year. And small businesses would qualify for tax credits to defray the cost of covering their workers.

*** The primary reason to propose tax subsidies is to keep the insurance industry alive. It is much less efficient than establishing a single universal risk pool financed by equitable taxes. Furthermore, the proposed subsidies would leave all but the wealthiest of us exposed to a potential obligation to pay about 20 percent of our incomes for health care. That is a burden that most would find very difficult to bear. ***

The inexorably rising cost of hospital and medical care is the underlying factor that drives up premiums, deductibles and co-payments. No one yet has an answer to the problem.

*** Balderdash! All sane economists agree that a single payer monopsony would solve the problem. Conservative economists might not like a government solution, but they agree that it would actually work. It’s time for the practitioners of the dismal science of economics to engage in normative economics. These are not only numbers we’re dealing with; they are about the lives and well being of people. ***

But the bills would launch an array of pilot projects to test new payment and health care delivery systems within Medicare. These include, for example, incentives to coordinate hospital and post-hospital care to head off needless readmissions, better coordination of care for the chronically ill, and incentives for doctors to provide a patient’s total care for a flat fee instead of charging for each test or service provided.

*** Continual improvement in health care delivery is an important goal, but it is in no way unique to the current legislative proposal. A single payer monopsony would have a greater capability of realigning incentives for optimal care. ***

The Senate bill would set up an independent board to spur the use of programs that save money or improve care — subject to Congressional veto. Optimists believe the savings might come quickly but this could still take many years. Without passing a reform bill, there is little chance of success.

*** See the first comment under “cutting costs.” ***

THE TIME HAS COME

For decades, presidents from both parties have tried in vain to reform the health care system and cover the uninsured. Still many Americans wonder, given the deep recession, whether it makes sense to do it now. The first thing to keep in mind is that the C.B.O. says that the reform bills are paid for over the next 10 years and would actually reduce future deficits.

The need is clear and the political timing is right with the Democrats controlling the White House, the Senate and the House. If this chance is squandered and Republicans gain seats, as expected, in the midterm elections, it could be a decade or more before reformers have another opportunity. Americans shouldn’t have to wait any longer.

*** Most of the major features of this legislation are not scheduled to begin for years, yet we are told that it is urgent that we pass this bill within the next several weeks. The urgency is not based on sound health policy but is based on the political goal of proving President Obama and the Democrats with a political victory well in advance of the next elections. That might be good politics, but it is an unforgivable neglect of duty that is being committed by our public stewards. The policies of a single payer Medicare for all program are much less complex than the dysfunctional model being foisted off on us with the misnomer of reform. Because of the toll of financial hardship, physical suffering and even death, there is urgency in the need to act. But we can act now and have the program fully up and running long before the dates proposed in the current legislation. The New York Times says that we are squabbling, by definition arguing about trivial matters. Racking up a political victory on the scorecard is trivial. Doing that while glibly accepting a system that will leave so many broke and uninsured is unconscionable. ***

NYT editorial, The Case for Reform: http://www.nytimes.com/2009/12/30/opinion/30wed2.html

The New Yorker's James Surowiecki on no need for private insurers

Fifth Wheel

by James Surowiecki

The New Yorker

January 4, 2010

The wayward, patchwork plan that we seem likely to end up with is probably a good reflection of the wayward, patchwork opinions that most legislators have on the subject.

So where’s the contradiction? Well, Congress’s support for community rating and universal access doesn’t fit well with its insistence that health-care reform must rely on private insurance companies. After all, measuring risk, and setting prices accordingly, is the raison d’être of a health-insurance company. The way individual insurance works now, risk and price are linked.

This kind of risk evaluation — what’s called “medical underwriting” — is fundamental to the insurance business. But it is precisely what all the new reform plans will ban. Congress is effectively making private insurers unnecessary, yet continuing to insist that we can’t do without them.

The truth is that we could do just fine without them: an insurance system with community rating and universal access has no need of private insurers. In fact, the U.S. already has such a system: it’s known as Medicare. In most areas, it’s true, private companies do a better job of managing costs and providing services than the government does. But not when it comes to health care: over the past decade, Medicare’s spending has risen more slowly than that of private insurers. A single-payer system also has the advantage of spreading risk across the biggest patient pool possible. So if you want to make health insurance available to everyone, regardless of risk, the most sensible solution would be to expand Medicare to everyone.

That’s not going to happen. The fear of government-run health care, the power of vested interests, and the difficulty of completely overhauling the system have made the single-payer solution a bridge too far for Washington.

http://www.newyorker.com/talk/financial/2010/01/04/100104ta_talk_surowiecki

Comment:

By Don McCanne, MD

So James Surowiecki joins the chorus of those of us who say that we have no need for private insurers and their unwanted service of segregating risk and setting prices accordingly, and that the most sensible solution would be to expand Medicare to everyone.

Yet he echoes the words of our progressive legislators when they first commend and then dismiss the Medicare for all model with the non sequitur, “That’s not going to happen.”

Time for our activism to reach a crescendo. We need to make it happen!

The New Yorker’s James Surowiecki on no need for private insurers

Fifth Wheel

by James Surowiecki

The New Yorker

January 4, 2010

The wayward, patchwork plan that we seem likely to end up with is probably a good reflection of the wayward, patchwork opinions that most legislators have on the subject.

So where’s the contradiction? Well, Congress’s support for community rating and universal access doesn’t fit well with its insistence that health-care reform must rely on private insurance companies. After all, measuring risk, and setting prices accordingly, is the raison d’être of a health-insurance company. The way individual insurance works now, risk and price are linked.

This kind of risk evaluation — what’s called “medical underwriting” — is fundamental to the insurance business. But it is precisely what all the new reform plans will ban. Congress is effectively making private insurers unnecessary, yet continuing to insist that we can’t do without them.

The truth is that we could do just fine without them: an insurance system with community rating and universal access has no need of private insurers. In fact, the U.S. already has such a system: it’s known as Medicare. In most areas, it’s true, private companies do a better job of managing costs and providing services than the government does. But not when it comes to health care: over the past decade, Medicare’s spending has risen more slowly than that of private insurers. A single-payer system also has the advantage of spreading risk across the biggest patient pool possible. So if you want to make health insurance available to everyone, regardless of risk, the most sensible solution would be to expand Medicare to everyone.

That’s not going to happen. The fear of government-run health care, the power of vested interests, and the difficulty of completely overhauling the system have made the single-payer solution a bridge too far for Washington.

http://www.newyorker.com/talk/financial/2010/01/04/100104ta_talk_surowiecki

Comment:

By Don McCanne, MD

So James Surowiecki joins the chorus of those of us who say that we have no need for private insurers and their unwanted service of segregating risk and setting prices accordingly, and that the most sensible solution would be to expand Medicare to everyone.

Yet he echoes the words of our progressive legislators when they first commend and then dismiss the Medicare for all model with the non sequitur, “That’s not going to happen.”

Time for our activism to reach a crescendo. We need to make it happen!